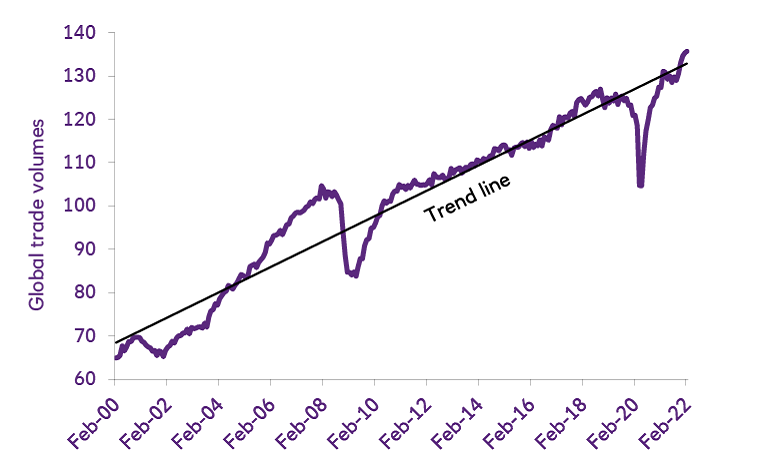

The war in Ukraine and covid surges across China have reverberated throughout the global economy and confront companies with yet more supply chain disruption. But the impact on global shipping and trade has been nuanced – and more muted than initially feared:

Shipping costs moderated in April across nearly all trade routes: they still remain high when compared with pre-covid levels (8.4 x January 2020 rates for global container shipping) but broadly below peak levels seen in August last year.

Lockdowns in China may have a more limited impact than feared: for now, bottlenecks appear limited to inland transport and production centres. When we look at the percentage of global container ship cargo capacity tied up due to port congestion, the latest data does show a rise in container ships waiting off Shanghai and neighbouring Ningbo-Zhoushan (the world’s third-largest port), but not to an exceptional degree as was seen during the Wuhan lockdown (early 2020) or last year’s port closures in Shenzhen (June 2021) and Ningbo (August 2021).

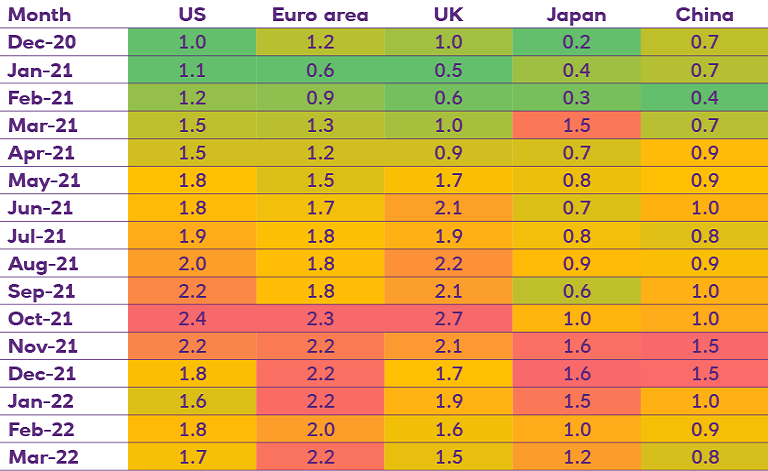

Supplier delivery time trends in April appear mixed: amidst raw material shortages, suppliers’ delivery times lengthened in the euro area and US, but the UK saw improvements despite facing the same headwinds (war in Ukraine, lockdowns in China).

Pressures on European supply chains are beginning to appear: a closer look at the NatWest Markets Regional Supply Chain Index (RSCI) below suggests that supply chains linked to the euro area took a hit in March following Russia’s invasion of Ukraine on 24 February, with the index rising to 2.2 times its long-term average. That rise in supply chain pressures came at a time when other countries saw them ease.

Supply chain pressures intensified in Europe in March due to the war in Ukraine