Economics

Monthly UK Economic Outlook: November

Our economists share their views on the key economic trends to watch in the month ahead.

02 Nov 2022

. 4 min read

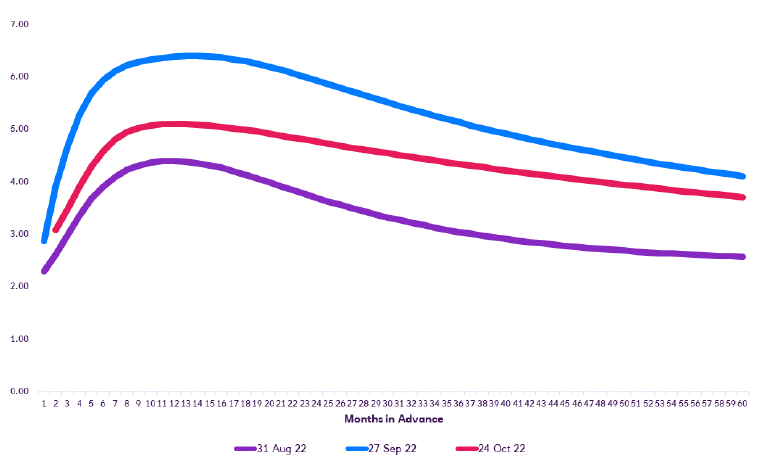

Tighter monetary and fiscal policy at home have compounded a difficult global backdrop of weaker growth and a stronger dollar. The squeeze on UK households’ income is likely to worsen amid rising borrowing refinancing costs, adding to the existing cost of living crisis. A potential scaling back of the energy support for households after April next year adds to the existing stress and uncertainty.