Sector trends

Agriculture news: wheat is where it’s at

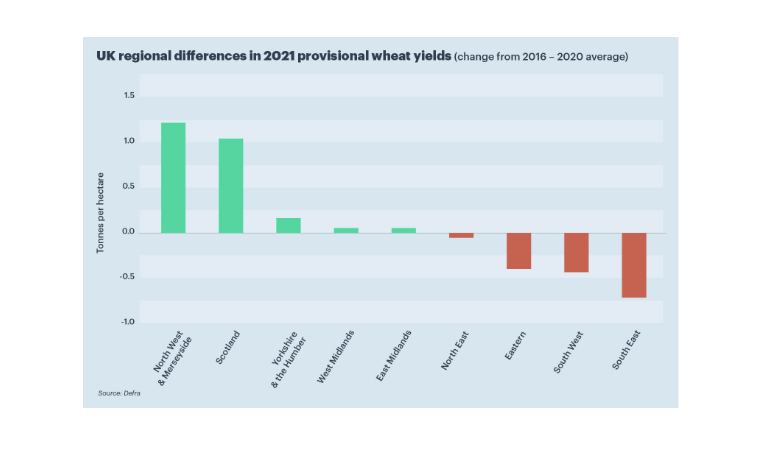

The Agriculture and Horticulture Development Board (AHDB), looks at changes in production for key crops and how they reflect the evolution of sentiment around inputs and prices.

08 Nov 2021

. 4 min read