With quantitative tightening (QT) set to kick-in from September and inflation and interest rates continuing to rise, debt servicing costs look likelier than not to swell. Government interest payments jumped to £19.4 billion in June 2022 – more than double the level a year earlier (£9.1 billion) – and reached £33.7 billion in the first quarter of this fiscal year (an increase of 82%). What’s more: we estimate that a 1% rise in RPI inflation increases government debt servicing costs by roughly £4 billion during this fiscal year and the next; a 1% rise in gilt yields could add around £3.7 billion over those two years; and a 1% rise in the bank rate could add as much as £11 billion.

Government’s capacity for additional spending is diminished – but politics poses risks

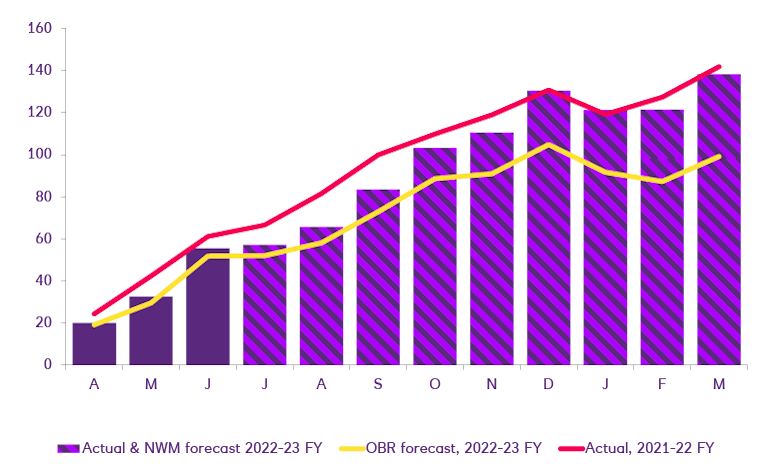

Larger-than-expected borrowing at higher costs and a challenging economic outlook will add yet more pressure on the government to keep its books balanced.

Ordinarily, this would impose limits on future fiscal policy loosening. But at the moment, the political landscape is anything but ordinary. This is all happening amidst a Tory leadership race where the two main candidates, Rishi Sunak and Liz Truss, appear to be flirting with the kinds of unfunded tax cuts (or spending increases) that would cause government finances to deteriorate further. The likely prospect of an election sooner than expected (May 2024), and by extension the possibility we could see fiscal giveaways to entice the electorate, only compounds those risks.

We don’t see this having a dramatic effect on the economic outlook. But anything that reduces the government’s future capacity to deploy fiscal firepower to help soften the blow of the cost-of-living crisis or a recession is worrisome. Especially if those challenges end up lingering for longer.

Upward pressure on bond yields

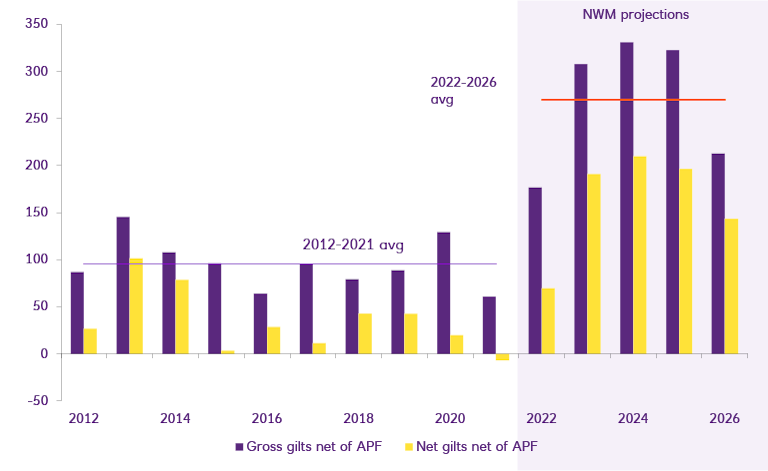

We think quantitative tightening, or QT, will combine with higher interest rates and more gilt sales to put upward pressure on bond yields.

We expect most of the government funding gap to be plugged by new gilt sales, with much of the funding likely to be needed ahead of the autumn Budget. The central government net cash requirement (CGNRC), the measure of borrowing that feeds directly into the government’s gilt issuance plans, is forecast to jump from £94.3 billion in April to £118 billion. That means the government will need to raise £23.7 billion, most of which via gilts.

Meanwhile, the Bank of England will be selling relatively large quantities of bonds (we estimate roughly £35 billion per year) back to investors.

QT will add to the gilt glut