Economics

The year ahead 2022: the post-pandemic economy and what it means for spending

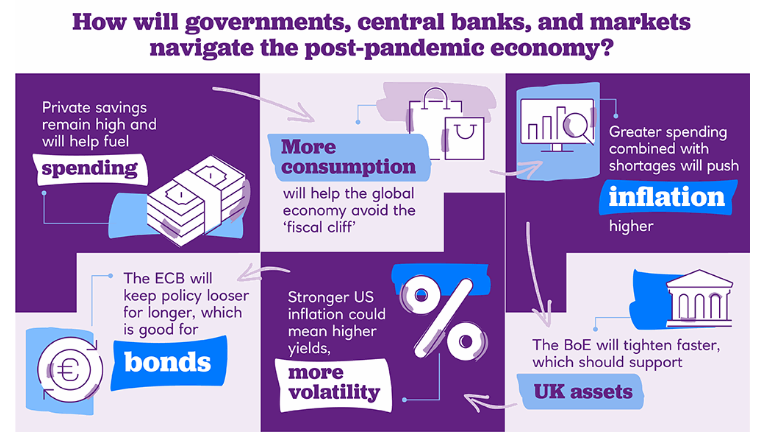

A closer look at how the decisions of governments and central banks could impact business over the coming months.

03 Dec 2021

. 3 min read