Economics

The year ahead 2022: how China’s policy shift could affect UK business

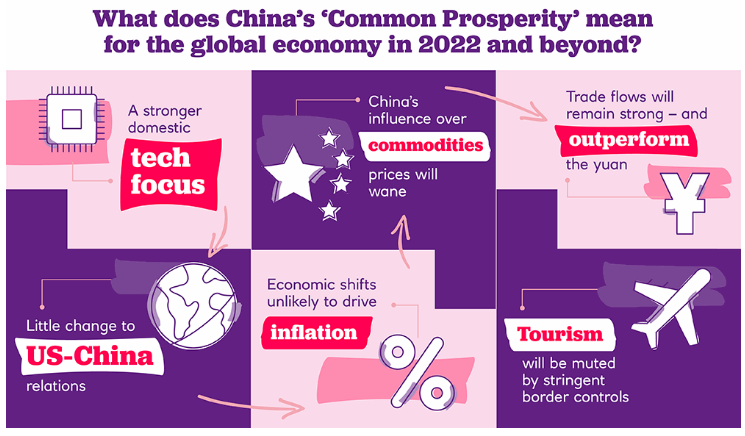

The People’s Republic has announced its aim to combat poverty and focus on the middle classes.

03 Dec 2021

. 3 min read

Here’s what its new ‘common prosperity’ policy will mean for the rest of the world.