Economics

Running on empty: four themes dominating the energy market outlook

Global energy markets are at a crossroads. How will the supply-demand imbalance, economic growth concerns, and the war in Ukraine influence where they go next?

02 Aug 2022

. 4 min read

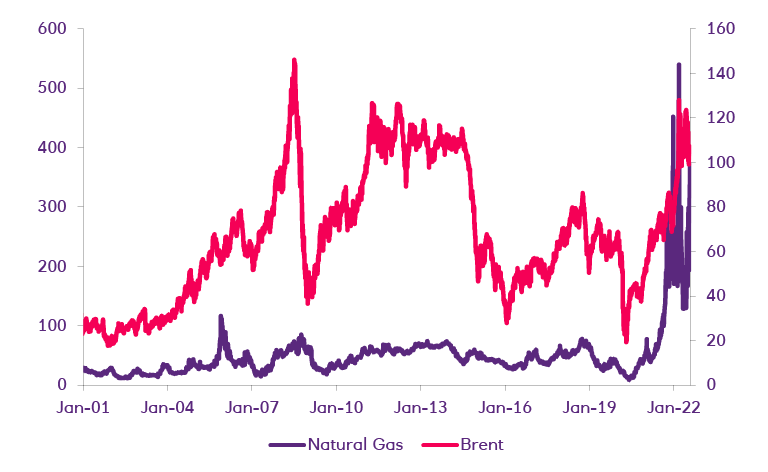

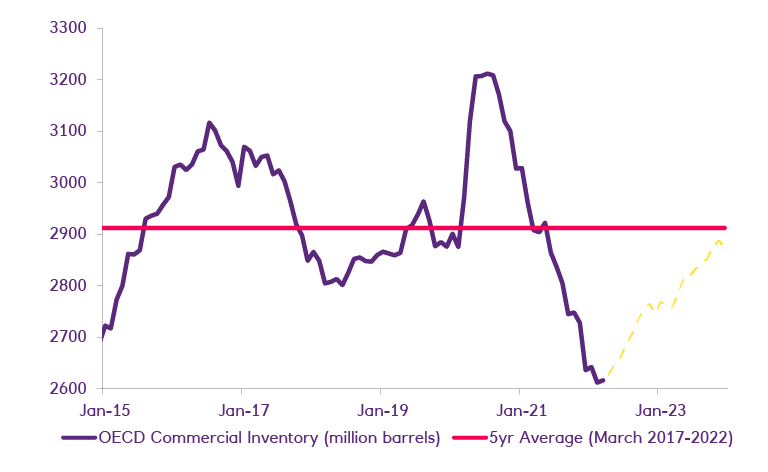

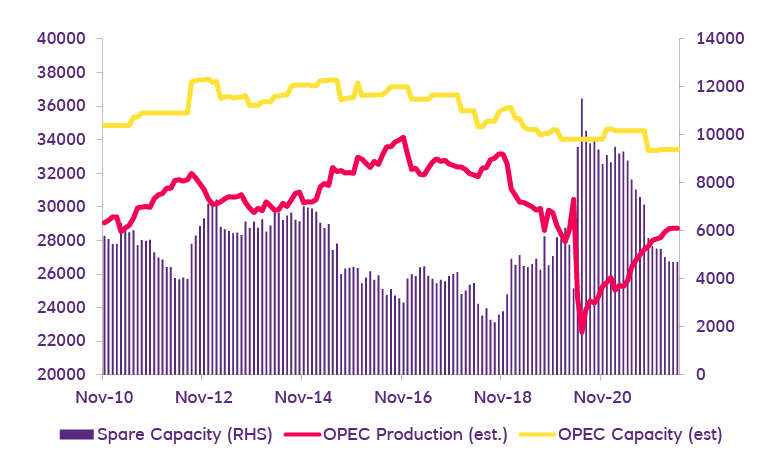

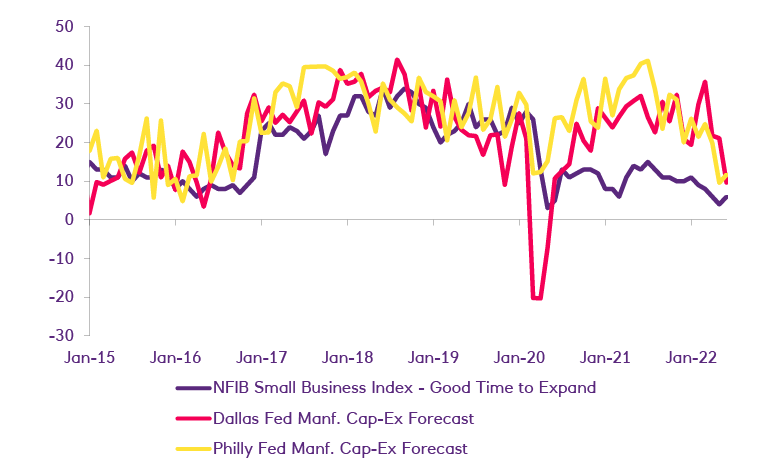

Like the global economy, energy markets face high levels of uncertainty. Current demand remains strong and strongly outweighs supplies, resulting in extremely tight markets and high prices. But concerns about economic growth are picking up steam, presenting future risks to both energy demand and prices. Even if demand falls, the dearth of supply is likely to remain supportive of energy prices in the second half of 2022, especially if the war in Ukraine continues.