Economics

Monthly UK economic outlook: September

Our economists share their views on the key economic trends to watch in the month ahead.

06 Sep 2022

. 9 min read

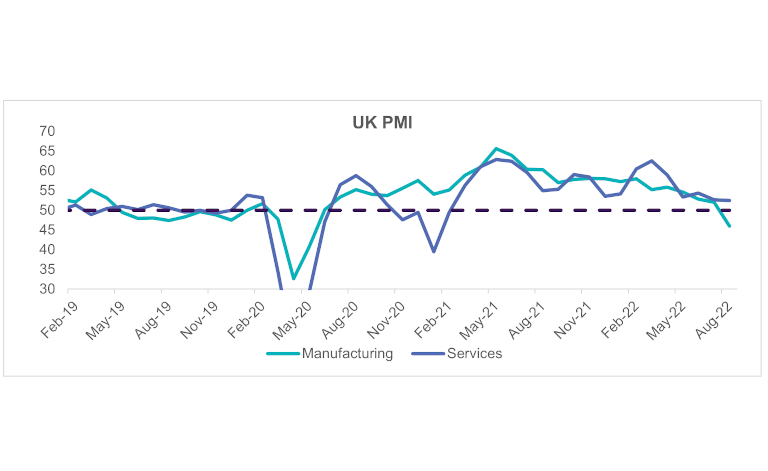

The challenges facing the UK economy continue to mount, but it’s not in recession yet. The PMI, a closely watched survey of business activity, continues to fall, but it remains above the crucial 50 level. And with relatively stable demand for consumer services, it points to some areas of resilience in the UK economy – for now at least. But for how much longer?