Economics

Monthly UK Economic Outlook: February

Our economists share their views on the key economic trends to watch in the month ahead.

08 Feb 2023

. 4 min read

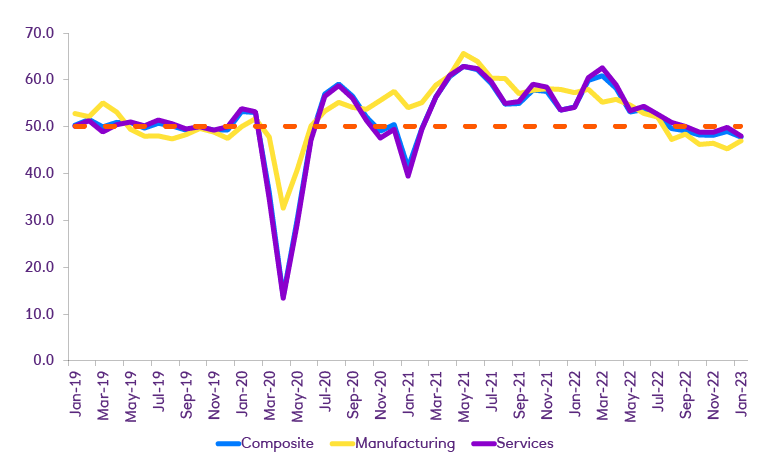

What a difference a month makes. An air of optimism has emerged at the start of the year, with a sense that 2023 may not be quite as bleak as had been envisioned only recently. The International Monetary Fund (IMF) has raised its forecast for global economic growth, while UK gross domestic product (GDP) was higher than expected in November, boosted by the services sector.