Economics

Monthly UK Economic Outlook: August

Our economists share their views on the key economic trends to watch in the month ahead.

10 Aug 2023

. 4 min read

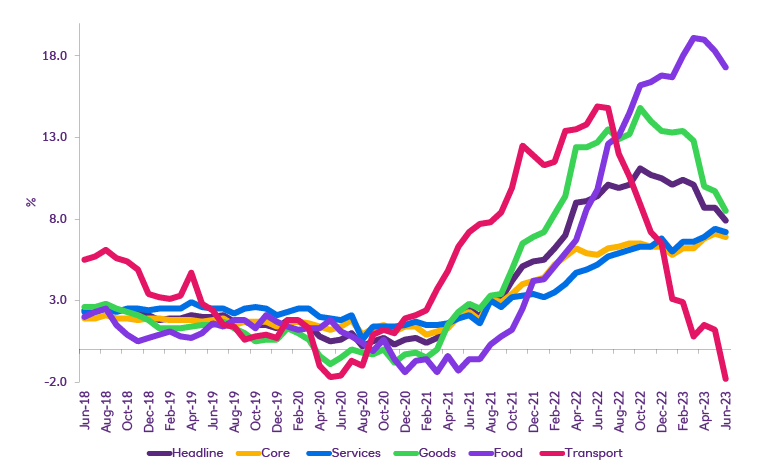

The UK economy has held up better than expected this year despite a rapid rise in interest rates and inflation outpacing wage growth. But over the past month we’ve seen evidence of inflation slowing, at long last.