Economics

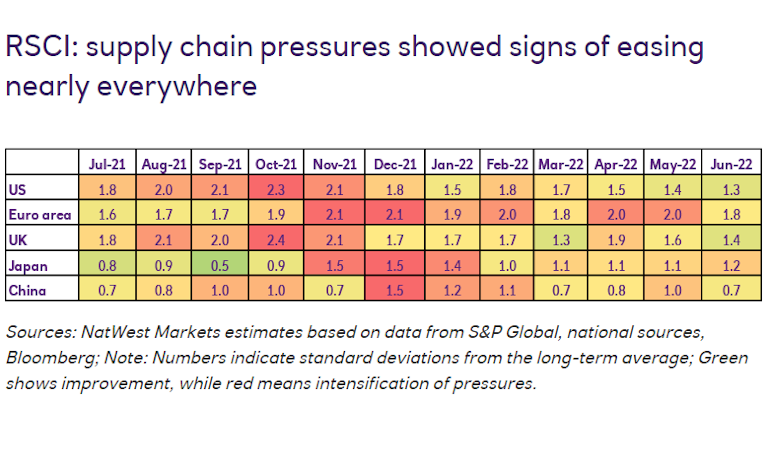

Tracking global trade: supply pressures show signs of easing amidst weaker demand

World trade activity edged up last month according to the latest data and supply pressures are finally beginning to show signs of easing.

12 Aug 2022

. 3 min read

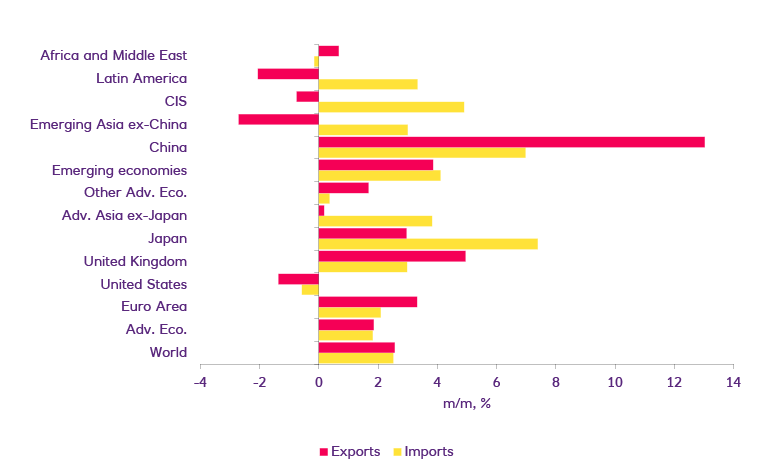

World trade is starting to show signs of a budding rebound: trade grew 2.5% month-on-month in May, after virtually no growth the month before, and 5.7% in year-on-year terms. Encouragingly, global trade volumes are now more than 10% above pre-covid levels.