Economics

Change or get left behind: Businesses adapt their plans as storm clouds gather, risks rise, and business confidence drops

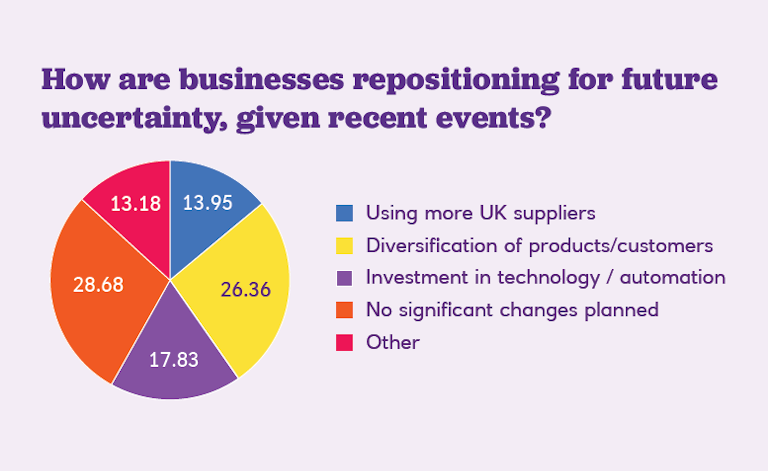

Uncertainty is riding high for UK businesses, and our H1 2022 survey of more than 100 businesses and meetings with dozens of customers in recent weeks confirm that the majority are planning big changes in order to address a rising tide of risks.

20 May 2022

. 4 min read

Inflation, geopolitical risk, post-Brexit woes, supply chain disruptions, and yet more Covid19 uncertainty – these are just a handful of the risks that our customers, and respondents to a wide-ranging survey of businesses, say they are facing. How are they responding to these risks? Here are some of the key takeaways from our conversations and from our H1 2022 survey.