Money matters

Investment Outlook 2025

In this article

Past performance should not be taken as a guide to future performance. The value of investments, and the income from them, can fall as well as rise and you may not get back what you put in. You should continue to hold cash for your short-term needs.

In 2024, the global economy showed remarkable resilience, recovering from the heightened levels of volatility and uncertainty in 2023. Global growth remained steady, avoiding the recession many had feared at the beginning of the year.

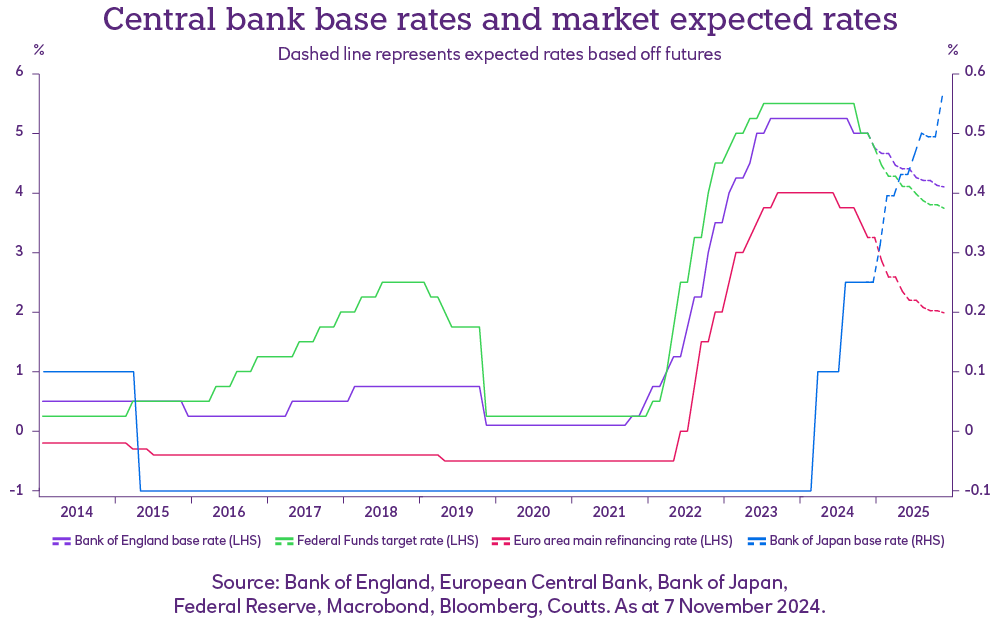

Instead, we witnessed many central banks from developed markets begin their interest rate cutting cycles. This came during a macroeconomic environment which differed from many of the previous cycles over the last 50 years as economies and jobs markets showed true strength and character. With inflation either approaching, or falling below, central banks’ 2% target, it was more ‘how much would central banks cut rates by’, rather than ‘if’.

Not all sectors shared the easing of rising prices equally. Goods sectors saw significant relief, however the services sector suffered ‘sticky’ price pressures throughout the year which central banks will continue to monitor closely. Central bank policymakers will have to find the right balance of managing inflation expectations while maintaining economic growth.

2024 did come with its uncertainties though. It was a year defined by elections, a new Labour government’s Budget and geopolitical tensions. In November, Donald Trump won the US presidential election along with the Republicans winning the majority of seats in Congress. This will make it easier for Trump to action legislation like tax reforms, deregulation plans and shifts on trade policies from next year.

For the UK, the rollout of the Labour government’s autumn Budget will be closely watched as fiscal policies, which were designed to stabilise public finances, could see inflation accelerate above 2% again. This has caused some concerns over how the Bank of England will manage the roadmap for bringing down interest rates in 2025.

Geopolitical risks such as ongoing dynamics between the US and China, as well as conflict within the Middle East and Ukraine, impacted market sentiment and global trade.

The investment team’s process at Coutts, the bank behind NatWest's investments, was focused on the robust health of US corporate earnings and strong consumer spending. By positioning our investments in ‘risk’ assets, such as equities and high yield bonds, our funds and portfolios benefitted from this.

Given that some uncertainties will persist in 2025, we will remain agile and diversified to navigate this complex landscape. The experts at Coutts will focus on the nuanced impact of policy shifts on stocks and bonds as well as sector-specific trends.

The past two years have seen the steepest rate hiking cycle in the past 40 years. This was efforts by central banks to control rising inflation which reached record highs across developed economies. Now that rising prices have remarkably begun to stabilise, the next two years will likely be a different story.

Many central banks have already begun reversing some of the hikes delivered between 2022 and 2023. This is likely to continue into 2025 should the battle with inflation avoid seeing average prices rise above the 2% target.

So far this year, the Bank of England has cut interest rates by 0.5% while the US Federal Reserve (Fed) and the European Central Bank have both reduced rates by 0.75%. At the time of writing, these three central banks are expected to deliver between two and five more rate cuts by July next year.

From the rate cuts we’ve seen already, there has been little economic pain as a consequence – particularly from the US. Job creations have been positive which has resulted in stable employment levels, and therefore consumer spending has sustained meaning positive economic growth. While it’s worth noting that the data supporting this has not been consistent throughout the year, recession fears which have cropped up occasionally throughout 2024 have largely receded in the last few months of the year.

Most of the other G7 countries share a similar story with the US. However, Japan has witnessed a different inflationary and rate backdrop compared to its G7 counterparts.

In the previous two years, while most other central banks were raising interest rates, the Bank of Japan held off from making any rate changes until this year.

The Bank of Japan may now be behind the curve compared to everyone else and so could potentially be an outlier during 2025 too.

Central banks have historically begun cutting interest rates in response to a deteriorating economy and weakening jobs market. This time around, it’s different.

Looking at the Fed’s previous rate cutting cycles since 1974, seven out of nine cycles have coincided with a US recession – where the economy contracts for two or more consecutive quarters. This is in parallel with markets on average being weak, falling by more than 10% from their recent highs. Examples include the 2001 dot com bubble and just before the Global Financial Crisis in 2007. Therefore, it’s not a surprise for stock markets to not perform well when central banks start lowering interest rates.

What makes this scenario different is that the US economy and jobs market remain positive, in contrast to previous cycles. Despite a recession not being completely taken off the table just yet, should one be avoided, continued consumer spending and growing corporate earnings would potentially see markets also continue to perform positively.

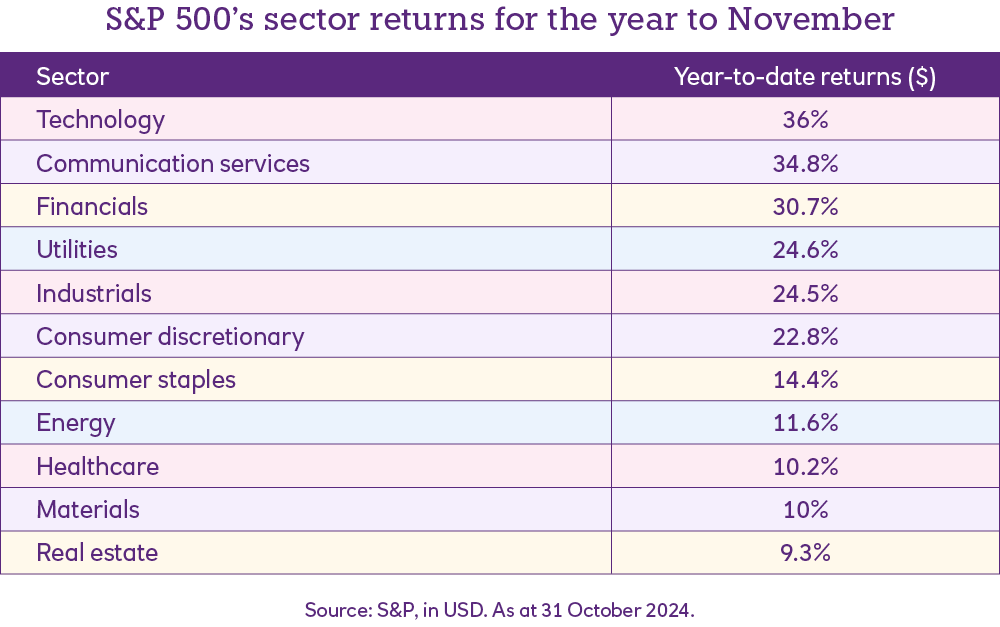

US earnings are expected to accelerate from next year, even with elevated interest rates. Growth is forecasted to reach 9% by the end of 2024, which could rise to 14% in 2025. US equities are also continuously reaching all-time highs throughout this year.

And where this earnings growth is coming from is broadening out. In early 2024, earnings growth had been led by the so-called ‘Magnificent 7’ – made up of Amazon, Apple, Alphabet, Microsoft, Meta, Nvidia and Tesla. Since then, and going forward, the proportion of companies delivering positive earnings has been growing while the Magnificent 7’s growth has been declining.

Therefore, markets have transitioned away from these mega-cap technology giants – which don’t typically do well in a higher interest rate environment – to more cyclical sectors. The transition of earnings growth and performance from a broader group of companies is, we believe, a healthier outlook for future equity returns.

With the global economy and corporate earnings maintaining solid growth, stock markets have performed well this year. This comes at a time when global inflation has been declining towards target and interest rates have begun coming down, resulting in both government and corporate bonds to earn their yield.

Against the backdrop of moderate economic growth and falling interest rates for much of the developed economies, our investment positioning is designed to lean into the positive outcomes of the business cycle while earning attractive bond yields.

Equity – Our investments continue to be weighted toward risky assets, specifically global equities, which should include multinational companies with strong profit-making potential.

Fixed income – Within the bond space, we lean away from Japanese government bonds as it is the one region where inflation and interest rates are rising rather than falling.

We are bullish as we enter 2025. Our short-term focus will be on continued moderate economic growth, rising wages and falling global interest rates which should all be good for corporate earnings.

Looking at the long-term, we take a less bullish approach. Valuations for risk assets are expensive. But with that said, they were also expensive a year ago which makes the point that valuations are famously not a timing tool.

This could cause central banks to pull on the brakes of their rate cutting cycles. Services inflation remains uncomfortably high and so could become increasingly sticky with interest rates coming down.

JP Morgan’s global manufacturing PMI – a leading recession indicator – is at levels suggesting a recession could be coming. The “Sahm Rule” – also a historically accurate indicator of recession – was triggered earlier this year when unemployment levels suddenly jumped. We have mentioned that this time around has been different for many other cases, and the same goes for these indicators which have been less effective than usual. But that’s not to say they are wrong.

Other risks exist too which we haven’t mentioned already. Rising oil prices, potential tariffs under the Trump presidency, and China heading towards a recession. All of these could have an impact on market performance.

While we are risk-on, we remain wary of risk. Therefore, our investment process is designed to address the potential outcomes of these scenarios should any of these risks begin to escalate.

Investing can sometimes appear complicated. Whether you're new to investing or an experience investor, we've got a range of articles to help you understand more about investing and the current investment landscape.