Money matters

Investment Outlook 2026: Resilience amidst turbulence

The value of investments and the income from them can fall as well as rise and you may not get back what you put in. Past performance should not be taken as a guide to future performance. Eligibility criteria apply. Advice and product fees may apply.

AI was the defining growth engine of 2025. Share prices of leading AI firms surged as investors embraced the transformative potential of the technology. Landmark deals in data infrastructure and semiconductor manufacturing fuelled further optimism.

Remarkably, AI capital expenditure contributed as much to US GDP growth in the first half of the year as US consumer spending – despite representing only 6% of GDP versus 70% for the consumer.

While concerns of an AI-driven valuation bubble emerged, they did little to dampen enthusiasm. For long-term investors, the sector’s promise outweighed near-term volatility.

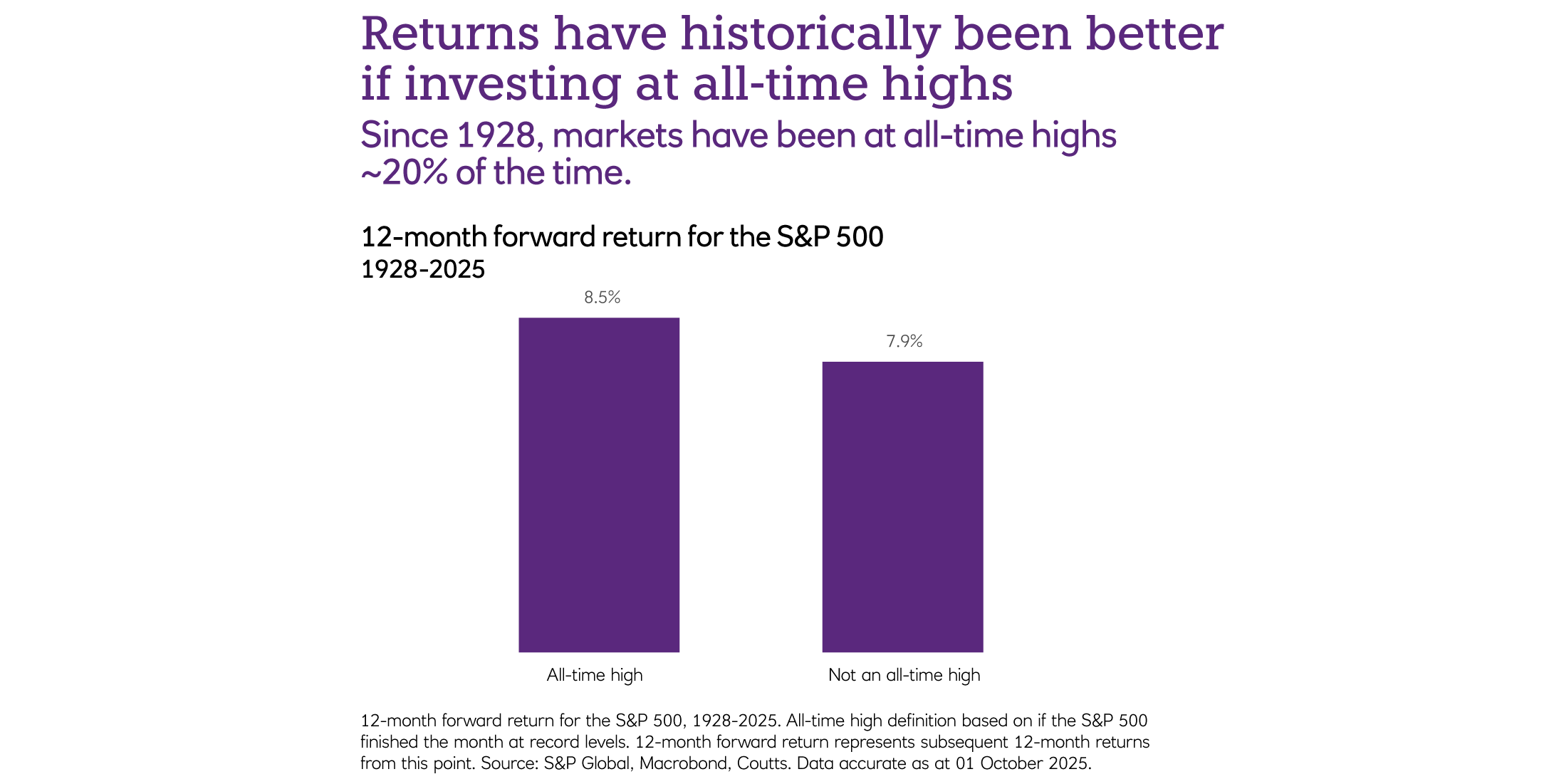

Another factor front of mind for investors was price. Investors faced the quandary of robust company earnings and solid economic fundamentals, but historically expensive valuations.

We examined these factors through our ‘Anchor and Cycle’ investment process – which balances long-term structural fundamentals (Anchor) with current business cycle dynamics (Cycle).

Our analysis found that equities, while expensive, remained worth the premium.

While valuations are a critical long-term determinant of returns, over the short term they can be a red herring.

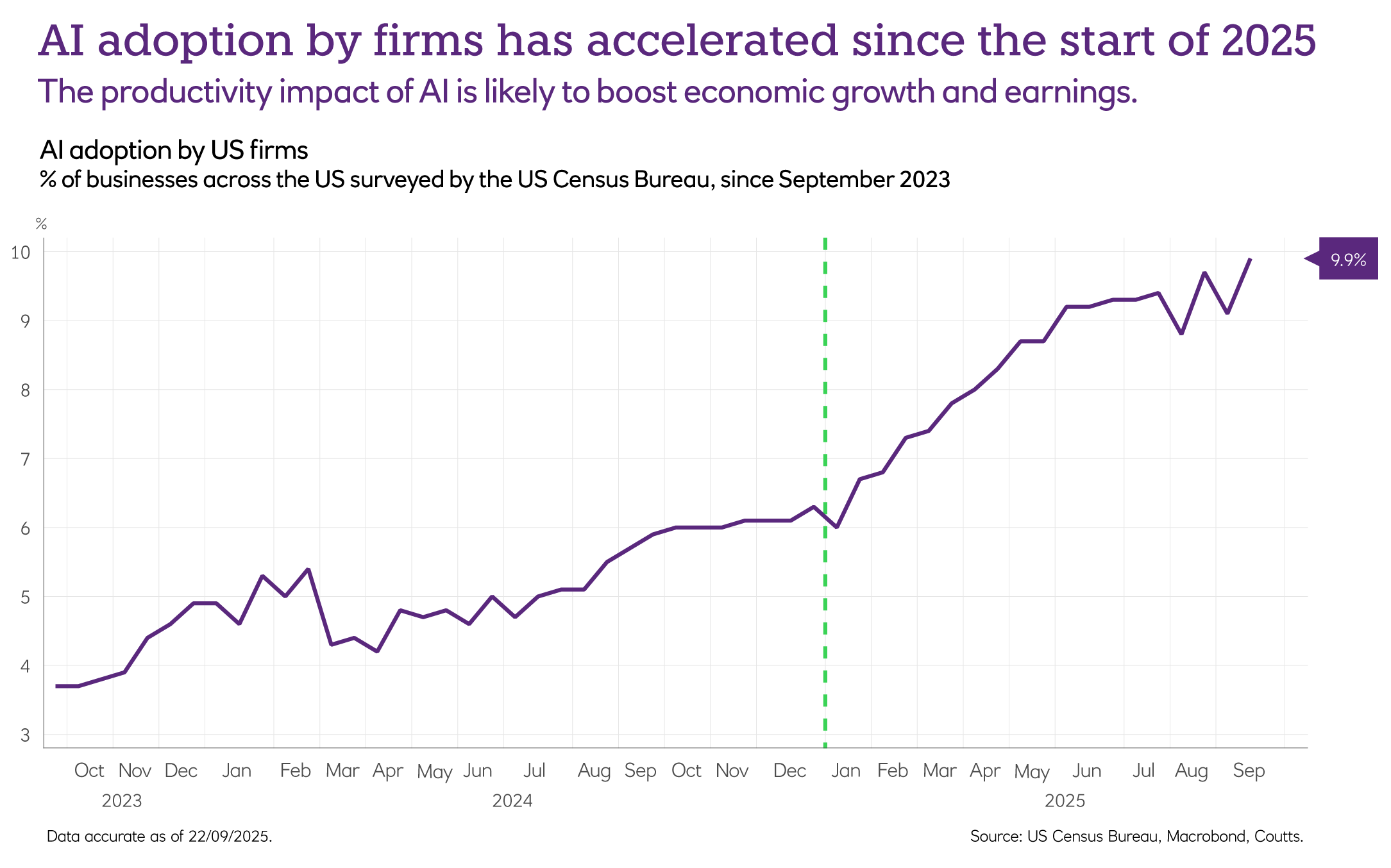

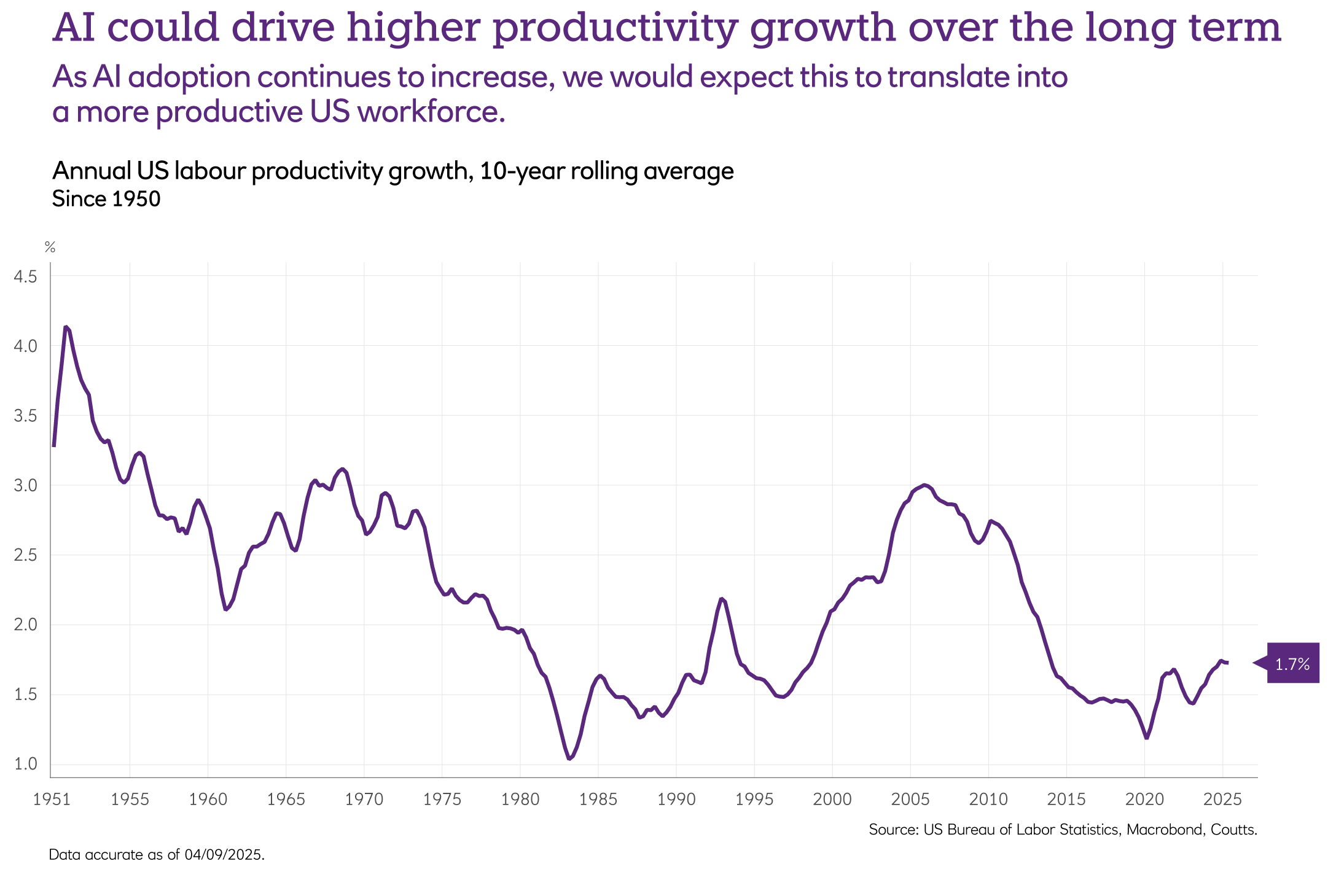

AI is a powerful engine of economic expansion, and capital expenditure within the sector is likely to continue. But adoption is still in its early stages. The chart below shows that, as of September 2025, only 9.9% of US firms surveyed had adopted it.

This leaves substantial room for growth, although we are likely to see some turbulence along the way.

Investors have been wrestling with the question of whether the US can remain ‘exceptional’, having outperformed global equities by 160% since 2015 (as at October 2025).

The weight of rising government debt, sizable fiscal deficits, a weaker dollar and America First foreign policy have been cited as examples of waning US influence.

But for us, America’s structural advantages endure, and we believe it will remain exceptional for the foreseeable future.

Private market investing has undergone a remarkable transformation. At the end of last year, global assets under management had tripled in size over the previous decade to $15.5 trillion, according to the Financial Conduct Authority.

This growth reflects strong demand from long-term investors seeking diversification beyond traditional public markets. Private market assets include private equity – ownership in non-public companies – and private credit, where asset managers or private funds provide direct loans to businesses outside public markets.

What sets private markets apart from traditional asset classes is their distinct underlying economic exposures, business models and economic sensitivities. As access improves, these opportunities could broaden the investible universe and enhance portfolio outcomes when combined with public market strategies.

The opportunities are striking, with far more private companies in the world than publicly traded enterprises. In the US alone, 99% of middle market businesses are privately owned, according to Ares Management.

As mentioned earlier, productivity is one of two key components in the engine of economic expansion, the other being demographics.

Demographics offer little support. According to the OECD, fertility rates across developed countries average 1.5 children per woman, well below the 2.1 needed to keep a population stable (assuming no immigration). This means we are likely to see ageing populations and smaller workforces – and the impact of this on public finances and economic growth could be sizeable.

This makes productivity critical, and AI could be the key that unlocks its potential.

Estimates for the economic growth impact of AI are wide. But a 2024 OECD study estimated it would contribute between 0.4 and 0.9 percentage points to annual US labour productivity growth over the next decade. PwC, meanwhile, predicts that AI could contribute $15.7 trillion to the global economy in 2030, with $6.6 trillion coming from productivity gains.

Volatility in the short term is quite possible and concerns about an AI bubble persist. However, unlike previous tech-led change, today’s AI leaders boast strong earnings and are funding expansion from vast cash reserves.

Like any paradigm-shifting development, AI comes with short-term pain, not least for workers displaced by new technologies. There has been some anecdotal evidence of this, with Fed studies showing slower job growth in recent years in AI-exposed sectors, as well as higher unemployment recently for young graduates.

Whilst job displacement is a risk, two things are worth noting.

Firstly, technological innovations have always changed job market composition. A typical UK worker today works around half as many hours as their counterparts in the mid-19th century.

And secondly, in the past, innovations have ultimately created new jobs to offset those made obsolete. Despite 200 years of innovation, we have not yet seen structural rises in automation. AI may be different, but that is not yet clear.

Despite the initial disruption of AI, we see huge potential for gains. And if the boost to productivity comes sooner rather than later, there should be nothing artificial about the benefits – over the coming year and beyond.