Sustainability

Financial Institutions ESG Monthly – 7 April 2022

Breaking down trending ESG* trades & themes to help Financial Institutions (“FI”) get ahead of the latest issues shaping the market.

07 Apr 2022

. 6 min read

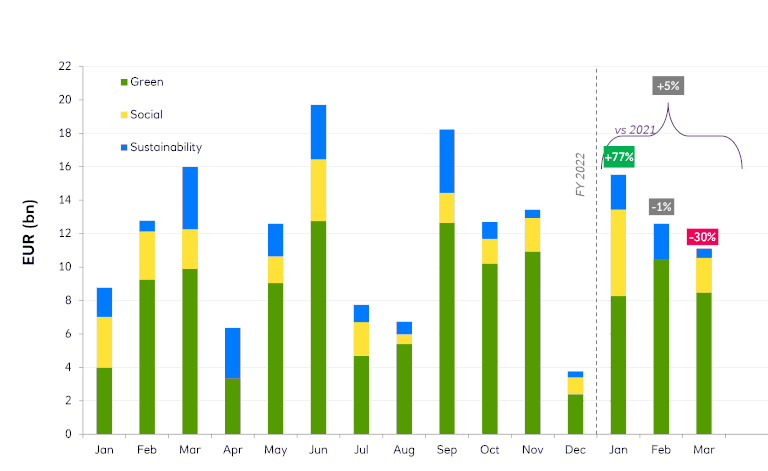

After a prolonged shutdown since mid-February, on account of market volatility, the FI Green, Social & Sustainability (GSS) market re-opened in the second week of March, with seven transactions totalling €5.1bn equiv. printed since 9 March.