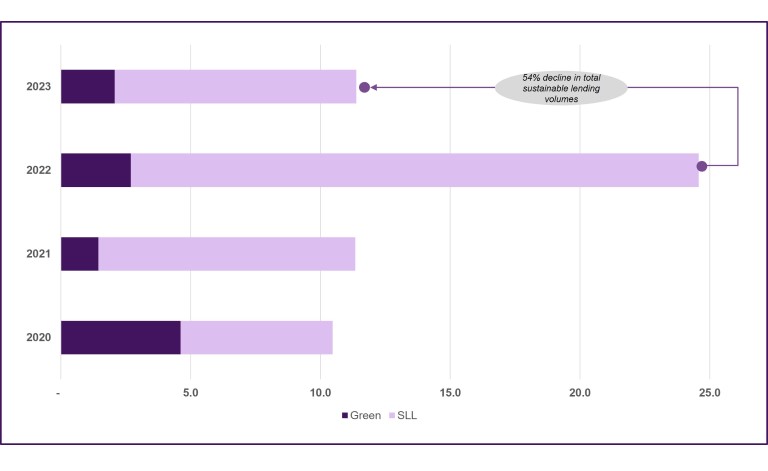

The following spotlight explores decarbonisation in real estate in more detail, based on the paper from Carbon Risk Real Estate Monitor (CRREM) and United Nations Environment Programme Finance Initiative (UNEPFI). This is the first of what will be a series of spotlights on ‘ESG considerations for Real Estate Investment’.

Decarbonisation of the building and construction sectors is critical to meeting our climate change objectives, however the scale of the challenge is significant: the sector accounts for c.40% of global emissions (including 11% from construction and 28% from operational activities) [1] [2], with estimates suggesting that it will take $5.2trillion over the next decade to decarbonise [3] the built environment.

Physical risks are something the sector has grappled with for many years (with these likely to be exacerbated as the severity and frequency of climate related incidents increases), however buildings not compliant with Paris aligned methodologies will be exposed to transition risks and also risk becoming stranded assets. The impact can be significant as summarised in the points below:

Transition Risk (#1): Declining attractiveness of submarkets due to increased vulnerability and exposure to higher costs.

Impact on Real Estate (#1)

- Lower demand (investor and tenants)

- Lower competitive advantage by increasing energy costs for properties with high-energy intensities]

- Reduced asset values may lead to a depressed market environment

- Decreasing market values

Transition Risk (#2): Increasing legislation focused on climate change - e.g. disclosure of climate risks, stricter building standards, CO2 pricing, carbon credits, etc.

Impact on Real Estate (#2)

- Tax increases e.g. CO2 tax

- Decrease in subsidies for certain technologies

- Additional costs from reporting requirements

- Additional investment costs to bring the real estate portfolio in line with national laws

- Enforced rules that properties can only be rented if they meet a certain energy standard

Transition Risk (#3): Risks to reputation and market positioning, with regard to stakeholder demand for real estate companies, where climate risks are included in the investment calculation.

Impact on Real Estate (#3)

- Loss of reputation if action is too late or if no action is taken

- Reputational risks for companies, that do not sufficiently consider ESG topics in their strategy

Source: CRREM 2022

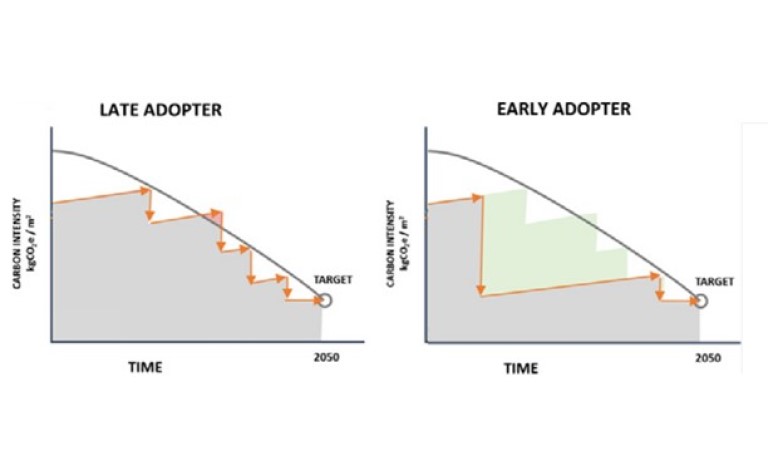

Articulating one’s net zero trajectory (with specific, bespoke short, medium & long term KPIs and targets along the way) should therefore be an immediate priority. These should focus on operational / asset level emission reduction given most buildings that will exist in 2050 have already been built [1]. To risk stranding assets, investors should engage actively and enable retrofitting & refurbishment, posing questions such as the below to identify gaps and opportunities (see more on p.20 here):

- Are our properties currently above or below the country average regarding energy intensity?

- Do we have sufficient energy consumption data and general property information to make strategic decisions?

- What is the carbon footprint of our energy consumption within our real estate holdings?

- What are the most relevant voluntary and regulatory requirements for decarbonization today and in the future?

- Which properties should be our priority for energetic retrofits and are we clear what the right timing is for interventions?

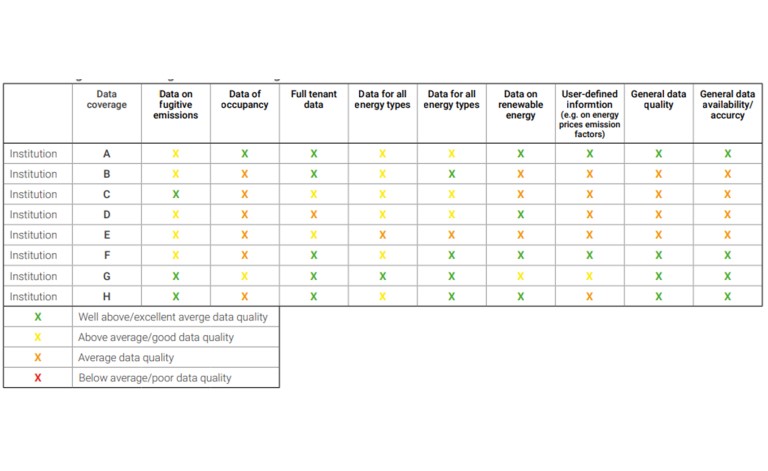

While these guidelines are largely acknowledged, the ecosystem is struggling to meaningfully accelerate its operational decarbonisation & transition, as it faces a number of headwinds with asset level data in particular. A survey of FIs by UNEP FI and CRREM showed the following (Figure.2):

- Only 41% of respondents had some of the asset-level information needed to carry out transition risk analysis.

- Less than a third (29%) said they did not have enough information available to carry out transition risk analysis.

- A quarter (24%) of institutions indicated that most information was available but only 6% reported that all asset-level information was fully available and accessible to them.

Figure 2: Results from a survey of FIs by UNEP FI and CRREM