The ECB ran a survey of the EU RFR (Risk-Free Rates) working group members to poll opinions, but the results were inconclusive. Notwithstanding this, LCH has decided upon a short delay to 27 July to ensure "a safe transition with the minimum of operational risks".

It is a balancing act between the risk of going sooner (ie June) when so many are still likely to be working from home (and operational, technology and front office staff are stretched) versus delaying, and potentially crowding up against the Fed Funds to SOFR discounting switch in October, creating delivery risk there. In the end a compromise of moving in July was reached, allowing a bit more time for preparation while not getting too close to the US date.

The issue is further clouded by a heated debate around swaptions. Swaptions are generally priced as if they were to settle via cleared swaps, meaning that they will use the discounting curves in use by CCPs at the point they are exercised. If those swaptions were entered into under the expectation of a different discounting curve, then there is a valuation difference and a case for an agreed compensation between the parties.

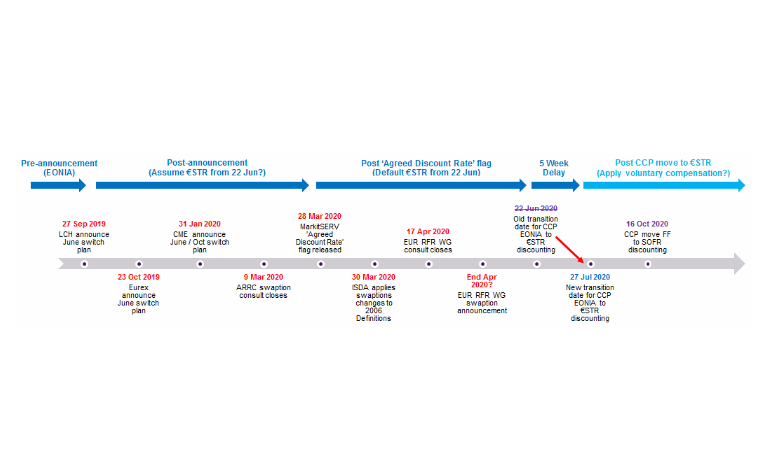

Since the end of March a new flag 'Agreed Discount Rate' has been added to confirmations, meaning there is now no doubt which discounting curve was used when entering into the swaption. The market convention since then has been to populate with €STR if expiring after 22 June, EONIA if before that.

But that leaves two areas of uncertainty: 1) will there be a compensation mechanism and how will it work?; and 2) assuming yes, what population of trades will it apply to? Since the end of March we can say with certainty that new trades expiring after 22 June are with €STR discounting, though CCP settlement will only match that now from 27 July. And pre September 2019 they were EONIA and some compensation may be due. The debate is around the population in the middle.

The change to the CCP date from June to July adds some further operational complexity, as swaption trades entered since the end of March (using €STR) and expiring before the new switch date, would have a payout that diverges from the price of the underlying cleared swap (as cleared swaps as of this date would still use EONIA discounting). There is a consultation from ECB on the compensation mechanism where closing date was extended to 17 April (the ARRC (Alternative Reference Rates Committee) consultation closed on 9 March).

See the timeline below of the key dates linked to the swaption question.

Whatever the pros & cons of the alternatives, the CCPs have now at least made a decision, and gone with a short delay to July.