- Upgrades to ESG scores are followed by equity outperformance: upgraded companies outperformed significantly, but downgraded firms didn’t see share value drop.

- Carbon intensity & emission cutting ambitions seem positively linked with credit default swaps (CDS): companies with lower emissions and greater ambitions to cut carbon output saw better credit performance.

- Policy appears to play a key role defining the relationship between financial performance and emissions: a comparison with a similar analysis of US utilities underscores the role of the Biden administration’s climate ambitions in persuading markets to punish high-emitting firms – but companies shouldn’t wait for policy before acting.

In previous articles, we’ve looked at whether the market has rewarded companies with good (or improving) environmental, governance and social (ESG) behaviours, including within the US utilities sector, financial companies, the oil & gas industry, and corporates more generally. In this article, we wanted to analyse the link between financial performance and ESG for large diversified energy companies – which of course have a relatively large carbon footprint. Let’s take a look at our findings.

Upgrades in ESG scores are followed by share price outperformance

We started off by looking at whether upgrades or downgrades in firms’ ESG scores (MSCI) are followed by outperformance or underperformance of their equities. These ratings provide a good overview of a company’s ESG credentials, so we were interested to see if changes make a difference to how investors allocate their capital to rated companies.

At the same time, it’s important to remember that these upgrades don’t just reflect improvements in firms’ climate strategies and carbon emissions – MSCI ESG ratings also account for factors such as corporate governance and social policies.

We looked at equity performance in the 90 days following a change in ESG score, because over longer periods other factors might drown out the effects of the change in the ESG score – in the short term, there are less likely to be other changes in fundamentals that would affect the firm’s or its peers’ performance.

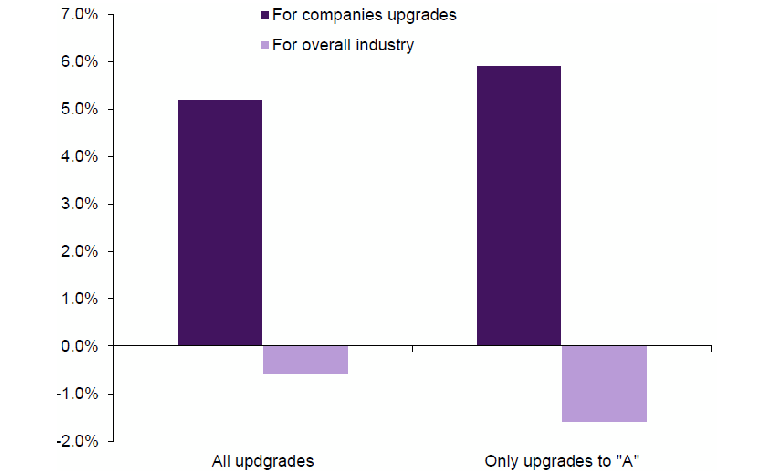

Looking specifically at energy firms with a market cap of at least $1 billion, there have been 19 instances of MSCI ESG score upgrades over the 12 months to the end of July, but only three downgrades over that period. Of the 19 firms that received ESG upgrades, we find that their share prices rose by an average of 5.2% in the three months following the change in rating. By contrast, the market-cap-adjusted industry average return over the same period was -0.6%. In other words, upgraded companies outperformed significantly.

Companies with ESG upgrades outperformed industry peers following the rating change (share prices %)

Companies with ESG upgrades outperformed industry peers following the rating change