VCMI supplements its Claims Code of Practice

The Voluntary Carbon Markets Integrity (VCMI) initiative released additional guidance to supplement its Claims Code of Practice. It’s now ready for use and companies can directly make claims against it.

According to the Code of Practice, the carbon credits a company uses must be of the highest quality, both to underpin the credibility of its claims and to help drive integrity across the market. VCMI defines high-quality carbon credits as those that meet the Integrity Council for the Voluntary Carbon Market (ICVCM) Core Carbon Principles [1] and qualify under its Assessment Framework. For further information on their collaboration see our COP28 update.

Each claim is ranked as Silver, Gold or Platinum and is based on the amount of residual emissions being offset.

Verra launches new methodologies

Verra released its new afforestation, reforestation and revegetation (ARR) methodology VM0047 at the end of September 2023 alongside a new leakage module, VMD0054 Module for Estimating Leakage from ARR Activities. VMD0054 must be employed by projects registered under VM0047. Generally, the methodology has been seen as an improvement, particularly in the dynamic baselines that test additionality and establish the crediting baselines at every verification.

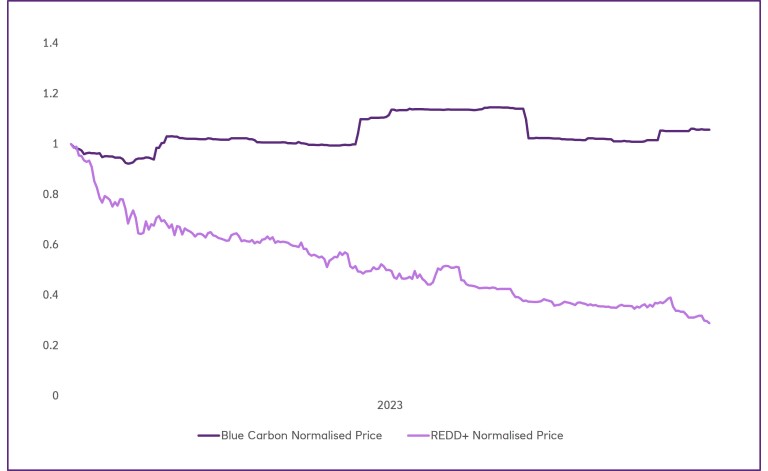

Verra has also unveiled its new REDD+ methodology (VM0048), which looks to prevent the over-crediting from REDD+ projects and the low prices of credits issued. The biggest change in what Verra calls a ‘revolutionary’ update is usage of Jurisdictional REDD+ baselines rather than developers determining their own; Verra will now lead on establishing project baselines. Data for these baselines will be sourced from high-quality service providers, in compliance with stringent accuracy requirements.

Unusually, the new methodology will be applied retroactively to existing projects that will have six months to comply before having to issue credits under VM0048. Indeed, projects using some older REDD+ methodologies (e.g.VM009) will have to provide compensation to credit buyers if VM0048 methodology results in a baseline with fewer credits.

Verra continues to evolve and respond to the need for the VCM and the increasing demand for integrity.

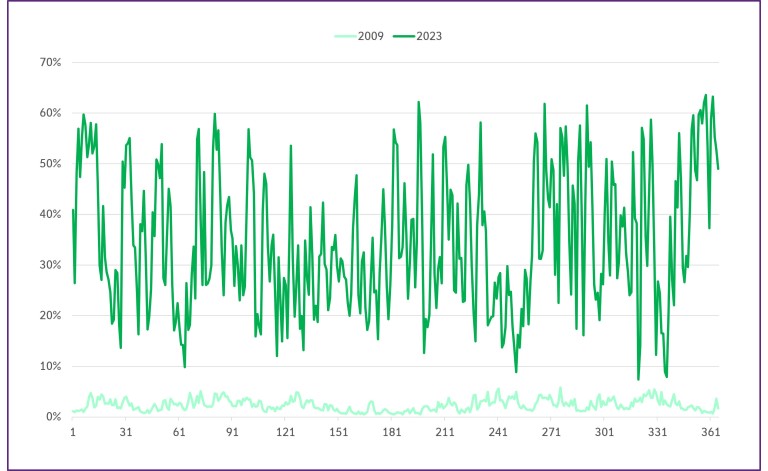

CORSIA Pilot phase ends and Phase 1 takes off

The CORSIA (Carbon Offsetting Reduction Scheme for International Aviation) is evolving from Pilot to Phase 1. The price of CORSIA (Carbon Offsetting Reduction Scheme for International Aviation) Pilot credits were between $0.50 per tonne, whereas prices of Phase 1 credits, which can only be purchased from issuances from either American Carbon Registry (ACR) or Architecture for REDD+ Transactions (ART), have cleared between $8.5 and $10.5 range (albeit with low volumes).

CORSIA Phase 1 holds substantial importance for the aviation industry. Like the Pilot, it is voluntary for countries but for airlines Phase 1 compliance is mandatory for international flights between participants. A total of 126 countries are participating in Phase 1.

The current uncertainties surrounding approved methodologies and market factors have hindered airlines from defining and implementing their Phase 1 CORSIA strategies. Encouragingly, increased clarity on methodologies is just around the corner, with further confirmations expected in the next two months.