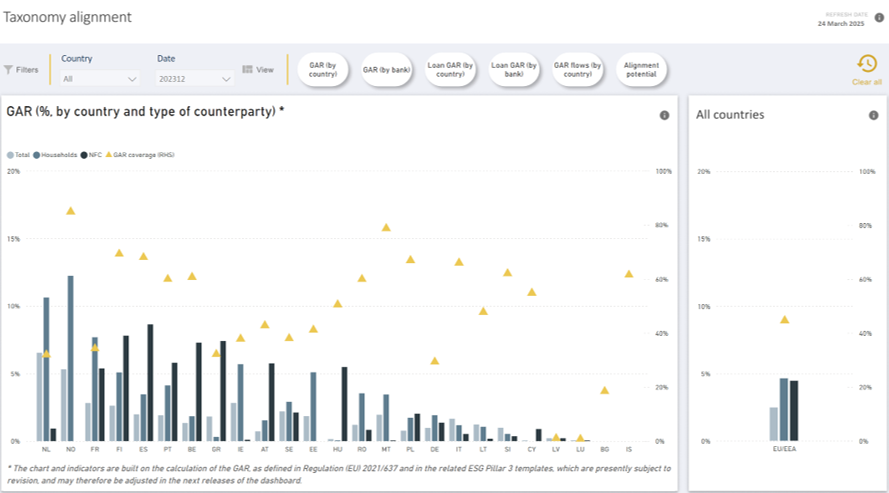

Based on information disclosed by banks as part of their Pillar 3 ESG disclosures, the new dashboard covers climate risk from both a transition and physical perspective, with indicators showing levels of green financing, based on alignment with the EU Taxonomy, in addition to considering internal definitions of green finance used by institutions. According to the EBA:

- The EU banking sector may be facing significant exposure to climate-related transition risk, with the data finding that exposure by banks to corporates from sectors highly contributing to climate change is above 70% in most countries, and 61% overall as of June 2024.

- Physical risk exposure appears to be much lower for banks than transition risk, with the indicator an average share of exposures in areas subject to elevated physical risk below 30% in most countries.

- The dashboard also found that the green asset ratio (GAR) remains low, with an average loan GAR across the EU/EEA of 6% as of mid-2024, although the EBA noted that this is partly “due to the fact that the economy is still under transition, with at this stage few activities being able to demonstrate alignment with the Taxonomy criteria”.

EU Platform on sustainable finance published a report with recommendations on criteria for new activities and first review of the Climate Delegated Act under the EU Taxonomy

The Platform on Sustainable Finance (PSF) has released [10] an independent report advising the European Commission on advancing sustainable finance through updates to the EU Taxonomy. The report focuses on two main areas: reviewing the technical screening criteria of existing economic activities in the 2021 Climate Delegated Act - particularly transitional activities - and developing new criteria for additional economic activities.

The aim is to enhance climate resilience and support the environmental transition by enabling more investments to qualify as taxonomy aligned.

Key recommendations include:

- Improving the usability and consistency of climate change adaptation and mitigation criteria

- Updating criteria to reflect new technologies and scientific findings

- Addressing gaps in the “do no significant harm” (DNSH) criteria

EU PSF published a report on monitoring sustainable capital flows highlighting growth rise in Taxonomy-aligned capex and primacy of debt financing

The Platform for Sustainable Finance (PSF) published [11] a report, “Financing a Clean and Competitive Transition: Monitoring Capital Flows to Sustainable Investments”, to gain insights on the state of capital flows to sustainable investments. The report analyses 2180 large listed European companies, primarily using EU Taxonomy data as of 2023. Key findings include:

- Momentum for sustainable investments: Taxonomy-aligned capex from large listed European companies reached €250bn in 2023, a 34% increase from the previous year

- Emergence of transition-related capital flows: €206bn potentially contributed to European companies’ transitions in 2023. These investments were defined as capex that was not Taxonomy-aligned but may support progress towards emissions reductions, provided that the associated companies had transition plans with enough elements of credibility

- The primacy of debt financing: Green bonds were the main financing instrument over the period, with annual EU issuance exceeding €200bn since 2021. Total outstanding green debt (including bonds and loans) reached €1.69tn in 2023

The report also asserts that the EU Taxonomy’s effectiveness “could be undermined if the scope of mandatory reporting is significantly reduced”.

EU PSF proposed a voluntary sustainable finance standard to improve SME access to green finance through simplified disclosures

The PSF published an independent report on streamlining sustainable finance for SMEs. The report suggests [12] a voluntary “SME sustainable finance standard” to help small and medium-sized enterprises (SMEs) access sustainable finance more easily and demonstrate environmental sustainability performance.

SMEs are vital to the EU’s green transition but face challenges in securing external funding due to complex regulations and limited resources. The new standard, inspired by the InvestEU programme, offers a simplified framework for banks and financial institutions to classify SME loans as sustainable and supports voluntary disclosures.

This streamlined approach would allow SMEs to share key climate-related performance indicators with financiers through an easy-to-use online tool. While initially focused on climate sustainability, the standard is expected to expand to other environmental goals, aiming to close the gap between SMEs and sustainable finance opportunities.

ESMA launched second consultation on draft technical standards for external reviewers under European Green Bond Regulation

The European Securities and Markets Authority (ESMA) released its second consultation paper [13] on draft technical standards under the Regulation on European Green Bonds (EuGB Regulation). The EuGB Regulation mandates ESMA to develop technical standards for external reviewers, which have been presented in two phases. The initial ESMA consultation paper was published on March 26, 2024, followed by a final report in February 2025. This latest consultation paper outlines five draft regulatory technical standards (RTS) and one implementing technical standard.

European Commission launched consultation on Industrial Decarbonisation Act to accelerate clean transition in energy-intensive sectors

The European Commission initiated a consultation process [15] to gather input for its forthcoming Industrial Decarbonisation Act (the ‘’Act’’), a central component of the Clean Industrial Deal. This initiative aims to expedite the decarbonisation of Europe’s energy-intensive industries, including steel, cement, and chemicals, while maintaining their global competitiveness.

European Commission opens consultation on EU ETS and Market Stability Reserve ahead of 2026 system review

The European Commission has opened a wide-reaching public consultation [16] on the EU Emissions Trading System (EU ETS) and its Market Stability Reserve (MSR). The feedback period is open until 8 July 2025. The results of the consultation will be used to inform future reviews of the EU ETS, which are planned for 2026. These reviews will assess the need for adjustments to the system, including potential changes to the way allowances are allocated or the way the system operates.

ESMA analysis reveals sustained inflow boost from ESG fund rebranding, with peak impact in initial quarters

On April 10, 2025, the European Securities and Markets Authority (ESMA) has published [17] its first report on trends, risks and vulnerabilities (TRV) for 2025 highlighting market developments, identifying market trends and comparing them over time and across markets.

The report found that adding an ESG term has a significant impact on fund inflows during the five quarters following the name change. The effect is most pronounced in the quarter of the change and immediately after, with inflows increasing by 2.2% in both quarters. In subsequent quarters, the effect remains relatively stable between +1.3% and 1.4%. The cumulative increase in inflows over the first-year amounts to 8.9%. The analysis was performed in the context of the implementation of the ESMA guidelines on funds’ names using ESG orsustainability-related terms.

EU bodies updated climate benchmark handbook and adopted regulation to strengthen oversight of climate benchmarks from 2026

- The EU Platform on Sustainable Finance published [18] an updated version of its handbook on EU Climate Transition Benchmarks (EU CTBs) and Paris-Aligned Benchmarks (EU PABs). The handbook consists of answers to FAQs on EU CTBSs and PABs, compiling responses from 2019, when the first version was published, and 2025. It also indicates which years the responses are from

- The Council adopted a regulation [19] amending the Benchmarks Regulation. Notably, it requires administrators of EU Climate Transition and EU Paris-Aligned Benchmarks to be registered, authorised, recognised, or endorsed to ensure regulatory oversight and prevent misleading ESG claims. The final text will now be published in the Official Journal of the EU and will apply from 1 January 2026.

ESMA published 2024 corporate reporting enforcement report highlighting supervisory actions on sustainability disclosures

ESMA published [20] a report on the “2024 corporate reporting enforcement and regulatory activities”, which provides an overview of the activities related to the supervision and enforcement of 2024 corporate reporting, including sustainability reporting, carried out by ESMA and national supervisors.

Enforcement actions were taken across several key areas such as disclosures relating to Article 8 of the Taxonomy Regulation, disclosures of climate-related targets, actions and progress as well as Scope 3 emissions.

EFRAG and CDP published mapping to align ESRS E1 with CDP climate disclosures and streamline corporate reporting

EFRAG and The Carbon Disclosure Project (CDP) published [21] a mapping between the CDP question bank and ESRS E1 (EU reporting standard on climate). The resource aims to demonstrate the degree of alignment between the two disclosure standards and help companies build reporting efficiency through the identification of data collection synergies.

The interoperability is reflected in areas such as transition plans for climate change mitigation, targets related to climate change mitigation, gross Scopes 1, 2, 3 emissions and internal carbon pricing.