A predominantly social problem

ESG investors have traditionally grouped tobacco with environmentally harmful industries such as oil & gas. But it is social (primarily health) issues that concerns investors most about tobacco.

The harmful effects of tobacco have been known for decades. According to the US Centers for Disease Control and Prevention (CDC), smoking-related illness costs over $300 billion each year in the US alone, with an additional $156 billion lost in productivity.

But health factors aren’t the only ESG aspects to consider. Product safety, labour standards and board ethics are also important. And from an environmental perspective, we shouldn’t forget the deforestation that occurs to make space for tobacco plants, the water needed to grow them, the problems caused by non-biodegradable cigarette butts and, of course, tobacco companies’ carbon emissions.

Regulation is becoming more stringent in the US and elsewhere

Tobacco companies have been the subject of tightening regulation globally for several decades, but the level of scrutiny they are coming under in the US is being cranked up even further. Under President Biden’s Cancer Moonshot Initiative, which aims to reduce cancer death rates by at least 50% over the next 25 years, there have been three major announcements about tobacco industry regulation in recent weeks.

First, the Food and Drug Administration (FDA) announced in June that Juul, an electronic cigarette company that is partly owned by Altria, one of the world’s biggest tobacco firms, is no longer allowed to sell its e-cigarettes in the US. In 2018, 75% of all e-cigarettes sold in the country were made by Juul, and even though this proportion had fallen to 43% by 2022, it is still a major player in the US market. The company, like many others in the burgeoning e-cigarette space, has been under federal scrutiny due to its efforts to get young people involved in vaping for several years.

Second, the FDA has proposed new rules prohibiting menthol cigarettes and flavoured cigars. Menthol cigarettes have been disproportionately popular among black smokers for decades, with marketing campaigns explicitly geared to black communities.

Finally, the Biden administration has announced plans to reduce the amount of nicotine in cigarettes to minimal or non-addictive levels. Nicotine is not the primary source of toxicity in cigarettes, but it makes it very hard to quit smoking. This policy alone is forecast by the FDA to result in the proportion of smokers in the US falling from over 12% today to just 1.4% by 2100.

Although there is debate about their ultimate impact, the FDA suggests these policies could result in 8 million tobacco-related deaths being prevented, 33 million people avoiding becoming regular smokers and more than $550 billion saved.

Should investors exclude tobacco from their portfolios?

Clearly, more stringent regulation of tobacco companies in the US is likely to reduce their financial returns. But that’s not the sole reason many investors choose to avoid the industry – many simply exclude tobacco firms from their portfolios from an ethical standpoint.

But is this the right thing to do? As ever, the answer is complicated. At NatWest, we’re strong advocates of engaging with firms to urge them to improve their practices. What’s more, there’s considerable divergence between companies in the industry in terms of how they’re trying to change. An investment strategy could focus on rewarding and penalising individual companies depending on how they perform with respect to investors’ desired outcomes.

Any investor considering allocating to tobacco companies also needs to consider the implications of new regulations. Will cigarettes become less detrimental to human health in the future? How will the new policies affect companies’ future revenue streams? The answers to such questions could have big implications on whether they choose to exclude tobacco firms from their investment universes.

Are ESG issues reflected in the performance of tobacco companies’ financial assets?

Given the wide-ranging ESG concerns about tobacco companies, we would expect them to trade at wider credit default swap (CDS) spreads (reflecting greater financial risk) than comparable firms, such as those involved in food & beverages. But is this the case? We performed some analysis from which we can draw the following conclusions.

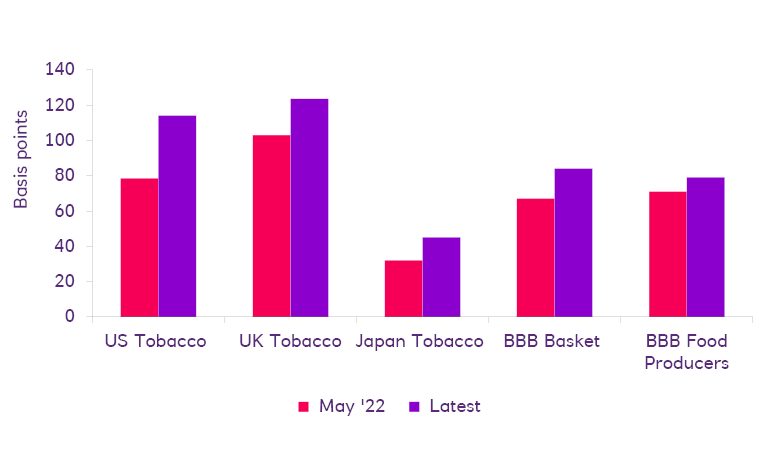

- Before the policy changes described above, large US tobacco producers were trading roughly in line with similarly rated large food producers, with five-year CDS spreads of around 75 basis points (bps). This was close to the average of 67bps for the BBB index.

- The largest US tobacco producer has traditionally traded only around 10bps wider than the BBB basket and has traded at tighter levels at times. This suggests that exclusions have had limited impact on credit pricing.

- European (especially UK) tobacco firms’ spreads have historically traded around 25bps wider than those in the US, while one Japanese company (with an A rating) trades at a much lower spread (32bps compared with 75bps for US firms). This suggests that the regulatory environment has a significant impact on credit spreads.

- The tighter regulations announced in the US have had a clear impact on spreads. As we can see in the chart below: whereas the overall BBB basket has widened by around 17bps over the past few weeks, spreads of US tobacco companies have increased by more than twice as much – 35bps – while the spreads of European and Japanese tobacco companies have essentially moved in line with those of comparable firms.

Five-year CDS spreads (basis points) for tobacco companies (May – June 2022)