Sustainability

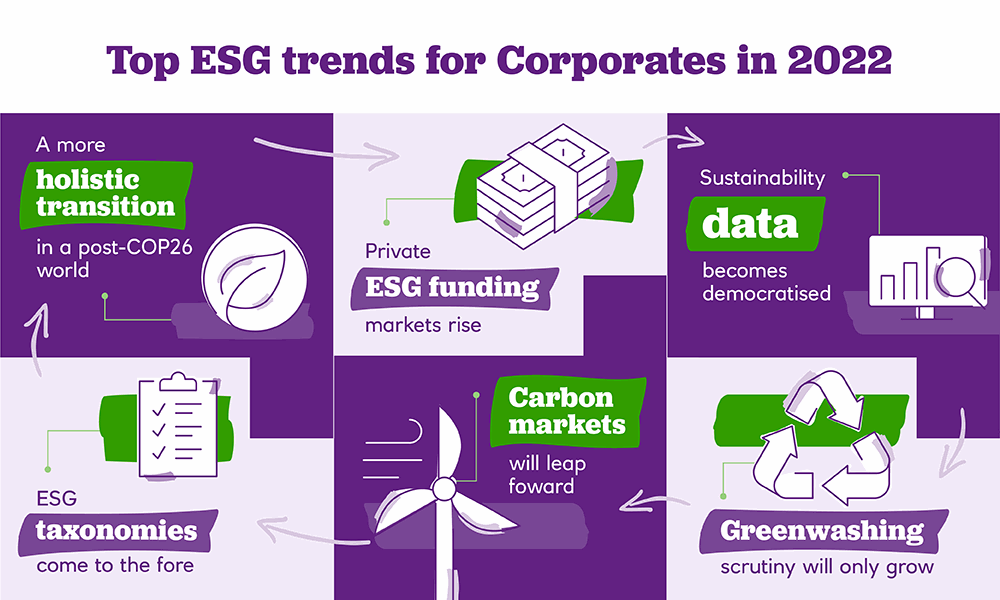

The Year Ahead 2022: Six themes set to shape the corporate ESG landscape in 2022

Sustainability continues to edge up the corporate agenda – so what does 2022 have in store?

22 Nov 2021

. 4 min read

Our specialists discuss six key themes that will dominate the corporate sustainability outlook in the year ahead.