Potential boost for the overall market

Firstly, such additional “top down” regulation tends to support, if not boost the overall momentum behind the asset class. This was certainly the case in China, where regulatory guidance on green bonds helped grow its market from virtually non-existent to one of the world’s largest in only three years (source: ADBI). While the European market is already more established, green debt still only makes up around 1% of outstanding Euro-denominated debt.

Green carrots…

It’s also likely that the EU GBS portion of the market will be considered a “gold standard” for green debt. Already, 77% of green bond investors consider such alignment “moderately” or “very” important for their investment (source: NatWest survey, 2021). If accounts put their money where their mouth is, that should create stronger “greeniums” for issuers adopting the EU GBS standards. Further potential regulatory incentives, such as the ECB (European Central Bank) applying lower haircuts for green bond repo operations, could stimulate this further in the future.

…and sticks

The GBS could also impact the legal framework of green bonds. Currently, there’s no effective investor protection post-issuance with risk factors pointing to the myriad of “green” standards. Non-alignment with EU GBS could conceivably be used as a trigger for an investor put option, thereby protecting accounts with dedicated green bond portfolios. It may, however, take a few years for issuers to get comfortable with such wording. “Softer” penalties are also feasible – e.g. exclusion from green bond indices or listing segments.

Issuer implications

Since 2020, 17.3% of European green bond issuers have announced their intention to follow the EU GBS (source: NatWest). We expect this number to grow steadily in the coming 2-3 years, as repeat issuers update their frameworks, benefit from wording utilised by “first mover” adopters, and as Second Party Opinion (SPO) providers offer this as a “core” part of their green bond service. Equally, it’s likely that the EU will tolerate a period of “grandfathering” of existing green bonds as market participants adjust to the new standards.

For framework changes, the main practical implications are likely to revolve around:

- Project use of proceeds alignment with the EU Taxonomy criteria

- Associated procedures conducted by the SPO provider

- Pre-defined metrics for allocation reporting

- Section on framework rationale

Green bonds are moving from gentleman’s agreement to a more contractual undertaking. The GBS is likely to be an important milestone in this journey.

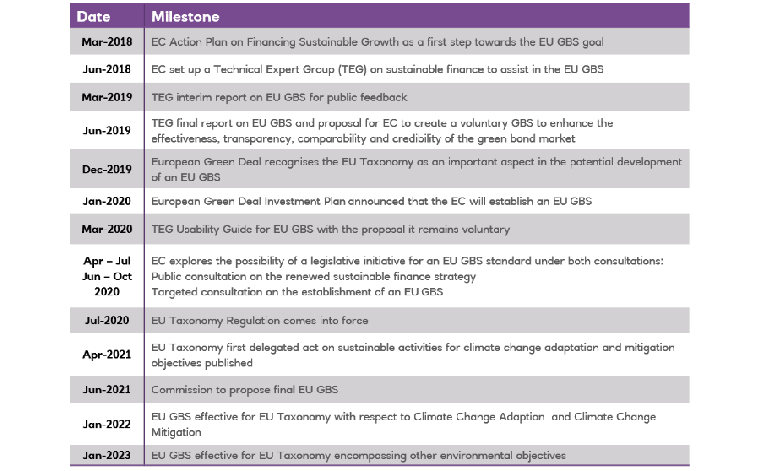

Overview of key GBS dates