1992: Launch of the UNEP FI, a partnership between UN Environment and the global financial sector to produce a global framework for addressing climate change and environmental deterioration through sustainable development.

1994: The United Nations Convention on Climate Change [UNCCC] comes into effect with the objective to ‘stabilise greenhouse gas (GHG) concentrations in the atmosphere at a level that would prevent dangerous anthropogenic interference with the climate system’. A total of 197 nations have signed the UNFCCC.

1997: The Kyoto Protocol emerges from the UNCCC, marking the first agreement between nations to mandate country-by-country reductions in GHG emissions

1999: Launch of the Dow Jones Sustainability World Index as the first global sustainability benchmark, evaluating the sustainability of companies.

2000: The first version of the Global Reporting Initiative (GRI) guidelines are published. Since then, the GRI has become the most world’s most widely used framework for sustainability reporting.

2003: Financial Institutions adopt the Equator Principles (EPs), a risk management framework for determining, assessing and managing environmental and social risk in projects. Currently, 111 Equator Principles Financial Institutions [EPFIs] in 38 countries have adopted the EPs

2006: Launch of the Principles for Responsible Investment

2007: The EIB issues the world's first Green Bond, labelled a Climate Awareness Bond (CAB)

2014: The Green Bonds Principles are established

2015: All UN Member States adopt the 17 Sustainable Development Goals (SDGs) to end poverty and protect the planet

2015: Nearly all nations adopt the Paris Agreement, a landmark environmental accord, during the COP21 in Paris promising to tackle climate change and move towards a low carbon future in order to keep the global average temperature rise this century below two degrees Celsius.

2015: The Spanish Instituto de Credito issues the first social bond

2017: Launch of ICMA’s Social Bonds Principles

2018: 631 investors representing over $37 trillion in assets sign the Global Investor Statement to Governments on Climate Change, calling on governments to adhere to the Paris Agreement and support the transition to low-carbon

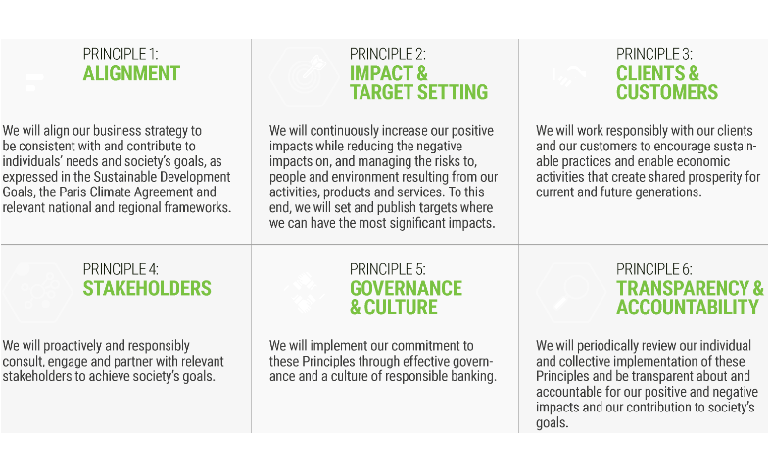

2019: The UNEP FI and 130 banks from 49 countries publish the Principles for Responsible Banking

2019: The EU Parliament and EU Council achieve political agreement on requiring ESG integration by financial market participants.