Sustainability

Sustainability-Linked Bond watch note: Q4 2021

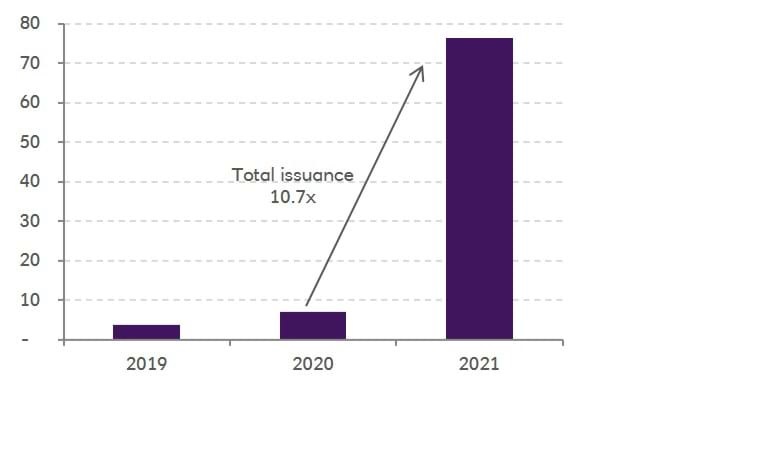

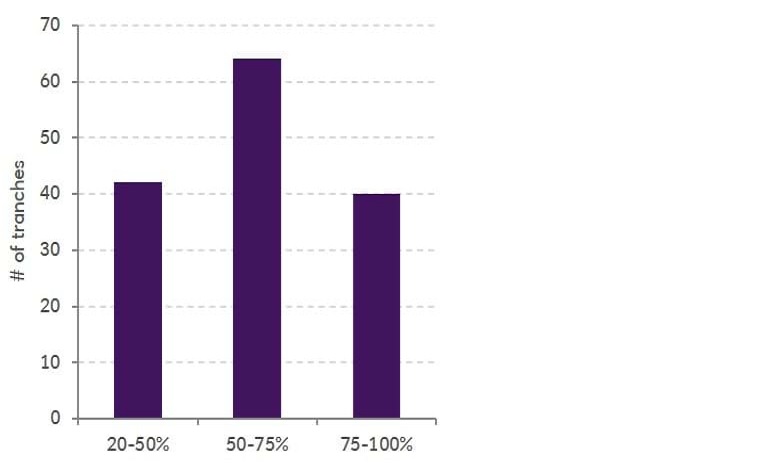

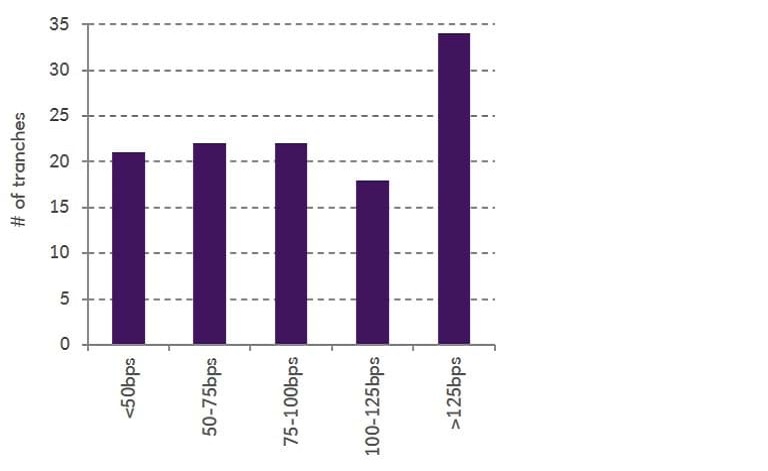

Sustainability-Linked Bonds (SLBs) made another push in Q4 with sales reaching EUR 76bn equivalent for FY2021, an increase of almost 11 times when compared to 2020.

14 Jan 2022

The market regained momentum after a small inflection in Q3, with issuances hitting a record high in November (EUR 17.5bn), even as most other types of ESG-labelled debt reached a plateau towards the year end.