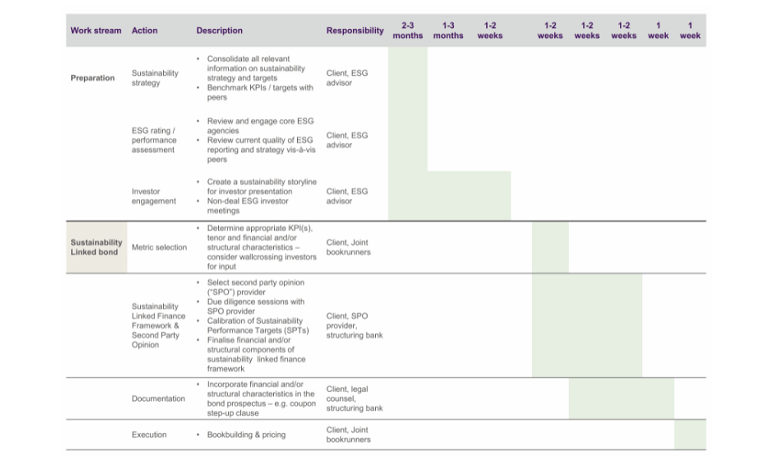

Selection of Key Performance Indicators (KPIs) determines issuer and lender credibility

The credibility of an SLB and SLL rests on the selection of one or more KPIs. The SLBP state that the KPIs should be material to the issuer’s core sustainability and business strategy and address relevant environmental, social and/or governance challenges of the industry sector; and be under management’s control.

Furthermore, the principles advise that the KPIs should be:

- relevant, core and material to the issuer’s overall business, and of high strategic significance to the issuer’s current and/or future operations;

- measurable or quantifiable on a consistent methodological basis;

- externally verifiable; and

- able to be benchmarked, i.e. as much as possible using an external reference or definitions to facilitate the assessment of the SPT’s level of ambition.

The SLBP encourage issuers to select KPIs that they’ve already included in their previous annual reports, sustainability reports or other non-financial reporting disclosures to allow investors to evaluate historical performance of the KPIs selected.

Similarly, the underlying KPIs for SLLs need to be aligned with the borrowers’ overall sustainable objectives and agenda. Typically, companies choose between one to five KPIs. While borrowers want to use KPIs, which are quantifiable and where the management feels confident they can meet the targets, it is important to formulate ambitious, ‘stretching’ KPIs, in line with the LMA Sustainability Linked Loan Principles.

Setting Sustainability Performance Targets

Calibrating one or more SPTs per KPI marks the second crucial step in structuring an SLB or SLL. The SLBP (and equally the SLLP) state the targets should be:

- consistent with the issuers’ overall strategic sustainability/environmental, social and governance (ESG) strategy,

- where possible be compared to a benchmark or an external reference, and

- be determined on a predefined timeline, set before (or concurrently with) the issuance of the bond.

- also, the issuer should disclose strategic information that may decisively impact the achievement of the SPTs.

Furthermore, the principles recommend that issuers set ambitious targets that, for example, represent a material improvement in the respective KPIs and be beyond a “business as usual” trajectory.

Detailing how the target setting exercise should be based on a combination of benchmarking approaches, the SLBP suggest to use:

- the issuer’s own performance over time (with a minimum of 3 years of measurement track record on the selected KPIs),

- the SPT’s relative positioning versus its peers’ where available (average performance, best-in-class performance) and comparable, or versus current industry or sector standards,

- reference to the science, i.e., systematic reference to science-based scenarios, or absolute levels (e.g. carbon budgets), or to official country/regional/international targets (Paris Agreement on Climate Change and net zero goals, Sustainable Development Goals (SDGs), etc.) or to recognised Best-Available-Technologies or other proxies to determine relevant targets across environmental and social themes.

Sustainability-linked bonds and loans to follow the same reporting standard and external verification process as use-of-proceeds bonds

Not surprisingly, as in nature a bond or loan, the SLBP and SLLP reflect the same expectations towards the reporting standard post issuance of a SLB and SLL as outlined in the GBP and SBP. Equally, the SLBP and SLLP advise issuers to seek external verification for their KPIs and SPTs.