Sustainability

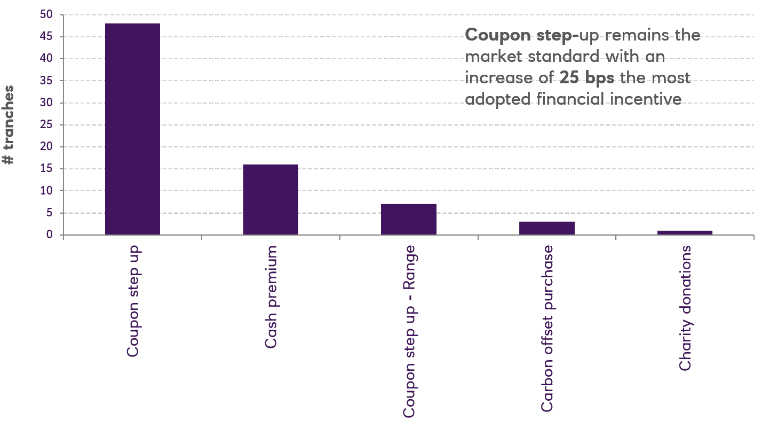

Step-downs: a step too far?

Recently, seafood company Thai Union became one of the first companies to issue a Sustainably-Linked Bond (SLB) with a coupon step-down element.

20 Jul 2021

Will we see more of such features? There are reasons to be sceptical: promoting such step-downs to investors is similar to involving the proverbial turkey in planning Christmas dinner – particularly, while credit spreads in most asset classes remain near record lows.