Sustainability

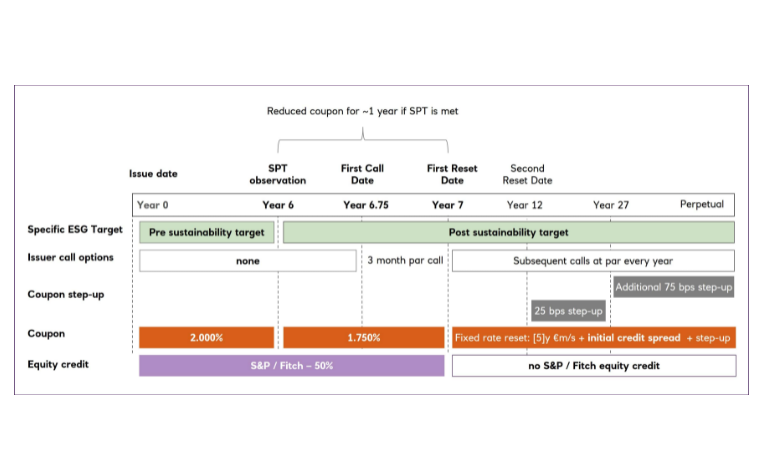

SLB hybrids - aligning non-call date and sustainability KPIs

The first article of this series introduced the potential interaction of two growing asset classes: Sustainability-linked bonds (“SLB”) and corporate hybrids.

14 Mar 2022

In this second article, we explore the Key Performance Indicator (“KPI”) structures seen in Senior bonds and how they could be overlaid in a traditional hybrid.