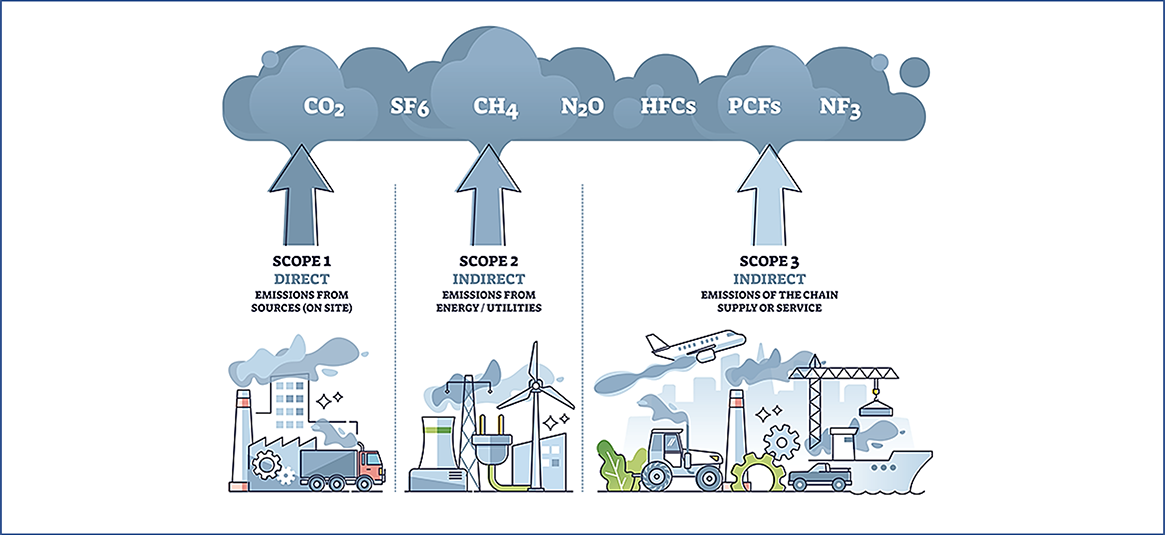

Scope 3 emissions – all those indirect emissions not included in Scope 2 that occur in the value chain of a company, including both upstream and downstream emissions – can account for a substantial portion of a company’s carbon footprint. However, not all Scope 3 emissions are created equal and by nature they can be complex to measure and to compare across different sectors.

So, what is the best way forward to report on Scope 3 emissions and setting a target? Which tools can help, and which issues will organisations most likely face? To get the views from ESG consultants and assurance providers as well as from investors on these topics, NatWest hosts Pietro Stimamiglio and Dr Arthur Krebbers from the Climate & ESG Capital Markets team at NatWest, welcomed:

Shaun Walden from DNV, Begum Gursoy from Sustainalytics, Isobel Edwards from NN Investment Partners.

Opinions shared by the expert panel included:

1. Minimum disclosure in scope 3 reporting can vary substantially across regions: Scope 3 reporting is further advanced in Europe compared to the US and APAC, however, there are still a lot of companies in Europe that only disclose minimal information about their Scope 3 emissions. This was also reflected by a short survey of the webinar participants: While 30% said that they have already defined and publicly disclosed their Scope 3 targets, 40% said that they are currently developing their Scope 3 target while another 27% admitted that they haven’t yet started to define a target.

2. Many companies are still in various stages of getting to a complete Scope 3 assessment. However, scope 3 reporting is iterative, and companies can improve and adjust in each reporting cycle as industry peers push other companies to report on Scope 3 on a more granular basis.

3. The multifaceted nature of scope 3 is generally recognised and corporate sustainability teams understand that of the 15 categories of Scope 3 emissions some are beyond the company’s control, or the company only has limited ability to deliver a meaningful impact. One of the challenges faced in many industries is that what is easier to report on does not match what is the most material type of emission for that company.

4. Companies are advised to seek external support to help assess and validate their Scope 3 reporting approach. Data quality and accuracy of reporting still present an inherent challenge for corporate issuers and investors. For example, Scope 3 is sometimes based on industry averages which makes it difficult to assess. But there is good news: a number of initiatives have launched to help companies measure their Scope 1, 2 and 3 emissions, with the Greenhouse Gas Protocol the most prominent example of support for companies seeking to tackle Scope 3 and to develop their Scope 3 reporting. Furthermore, ESG data providers, ESG assurance providers and other specialist firms are set-up to help investors and companies to capture, assess and verify data through smart technologies such as block chain or tagging.

5. There are several alternatives and proxies to full Scope 3 KPIs for Sustainability-Linked financing: Companies can outline the most material areas impacting their Scope 3 emissions and then set KPIs to address specifically all or some of those areas – e.g. the reduction of landfilled products, increase in recovered products, increase in electric vehicles used, waste reduction, increase in sustainable materials purchased in the supply chain, percentage of engagement goals reached.

Watch the full webinar

To watch the replay of our ESG stakeholder panel webinar, please click this link