Sustainability

More government intervention to get the market down the green path...

BoE set to green its Corporate Bond Purchase Scheme.

02 Sep 2021

. 5 min read

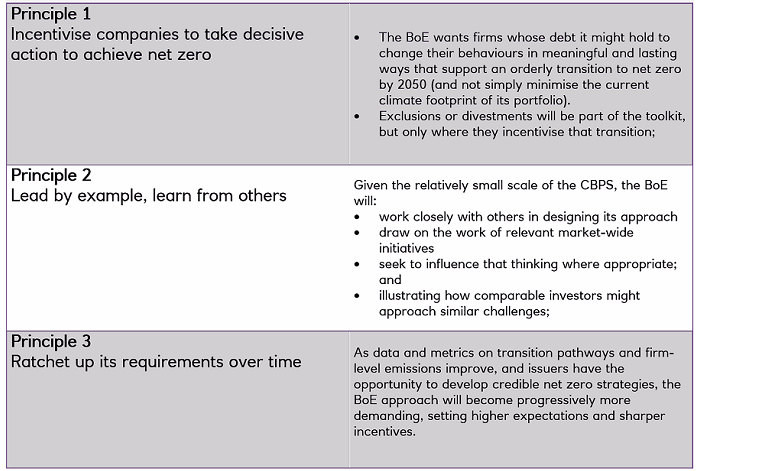

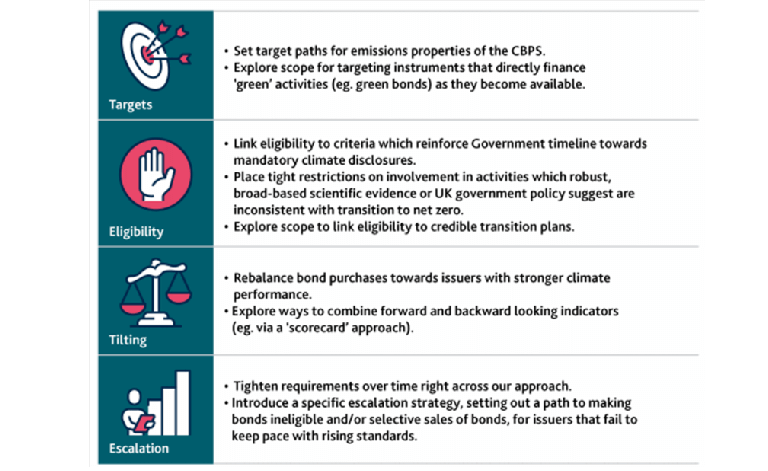

In a widely covered speech, Bank of England (BoE) governor Andrew Bailey had already doubled down on promises to ‘greenify’ the BoE’s policies after Chancellor Rishi Sunak, in March, updated the Monetary Policy Committee’s (MPC) remit to include supporting the transition to a net zero emissions economy.