Sustainability

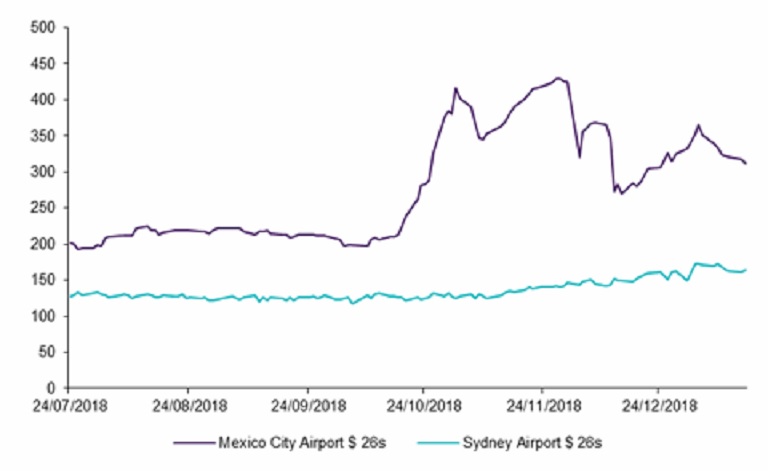

Mexico City Airport: 'The green bond that was no longer'

When Mexico City Airport Trust issued $6 billion of green bonds in 2016 and 2017 in order to finance the construction of a new airport, the New Mexico City International airport, the investor community welcomed a green issuance from a sector that hadn’t been linked to sustainability and the green financial markets before.

16 Jan 2019

The bonds exceeded ICMA Green Bond Principles (“GBP”) standards, obtaining a second party opinion from Sustainalytics as well as green instrument evaluations from rating agencies Moody’s and S&P.