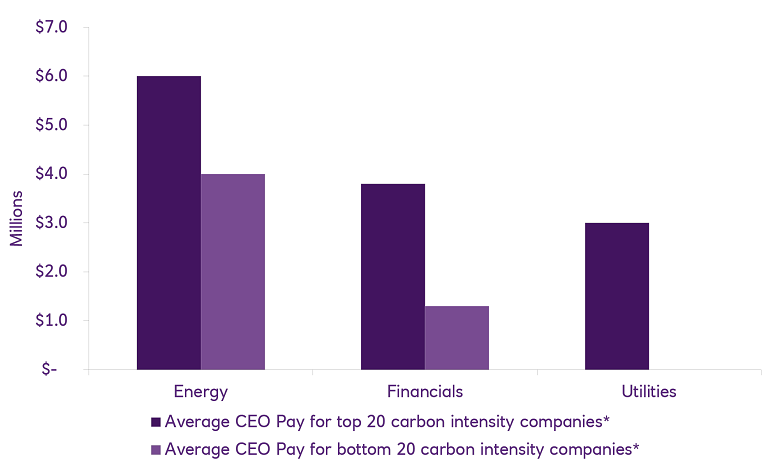

To see whether ESG-linked executive pay influences sustainability progress, we analysed carbon emissions intensity for 916 companies that have implemented such policies globally between 2015 and 2019 (381 utilities, 441 financial companies, and 94 energy firms) using salary and sustainability data from MSCI (we excluded companies for which data was incomplete).

Unfortunately, we found that companies with higher absolute emissions intensity tend to pay CEOs significantly more than companies with lower emissions, across the three industries (see chart below).

On the face of it, this would suggest companies linking ESG performance with CEO pay are not effectively bringing about the kind of progress on sustainability they aspire to, but it’s important to take these results with a grain of salt. They lack detail on how specific companies align individual metrics to CEO compensation, and only indicate whether the company has incorporated links to sustainability performance in its pay policies. The data neither defines the type of target, nor takes into consideration the incentive’s effectiveness either when a company announces the linkage or across time. Clearly, the data needs to improve. This presents some hard truths for companies, investors and other stakeholders: the clear need for accountability and transparency.

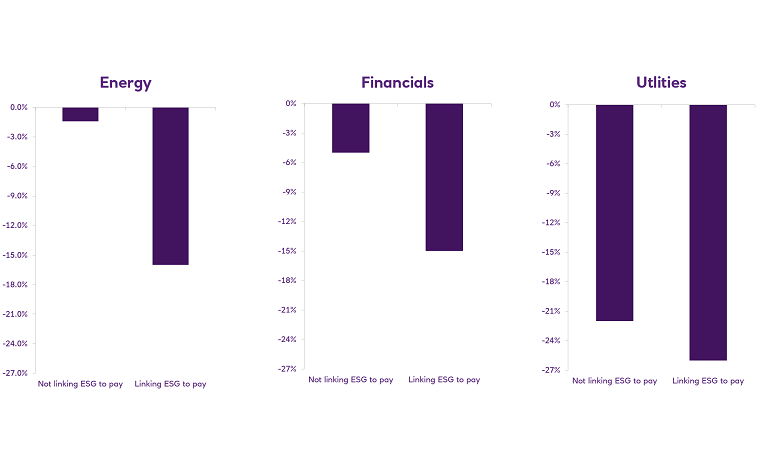

What about the link between executive pay and changes in carbon intensity over time? We compared companies that do and don’t tie executive pay to ESG performance between 2015 and 2019.The results are consistent and positive (see below): across the three sectors we analysed and excluding a handful of outliers, companies that tied executive compensation to the achievement of ESG performance improvements reduced their carbon emissions more than those that didn’t.