Sustainability

How are issuers of various ESG-labelled bonds (and none) different?

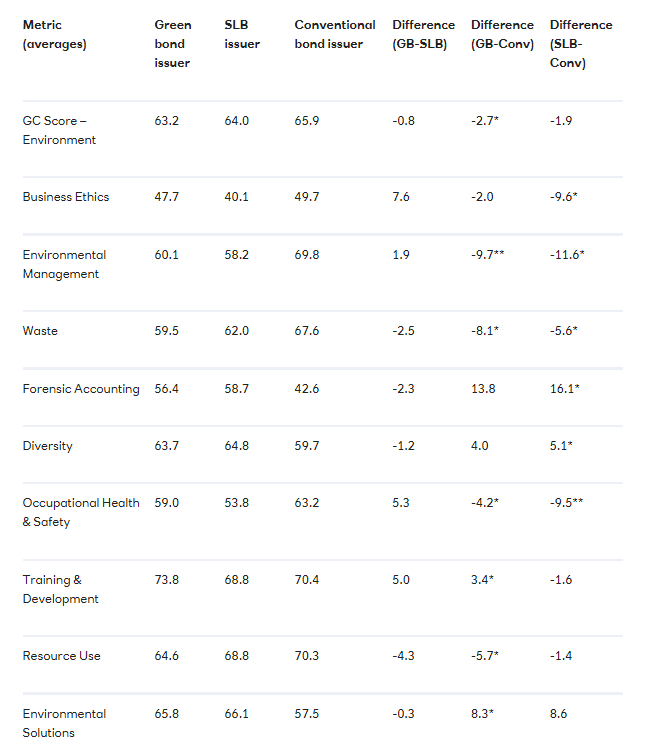

There’s a lively debate around the wider benefits of issuing sustainability debt, and, indeed, whether those benefits are more for a green (or other ‘use of proceeds’) instrument or a sustainability-linked instrument.

04 Jan 2022

With the European corporate market for both structures having grown rapidly over the past year, we have conducted some initial analysis on this topic. For this purpose, we have utilised the full range of Arabesque S-Ray ESG scores for listed issuers of green, sustainability-linked and conventional bonds. While the sample sizes and period are necessarily limited, our indicative analysis leads to two observations: