Sustainability

Green recovery bonds: where do companies invest money post-COVID?

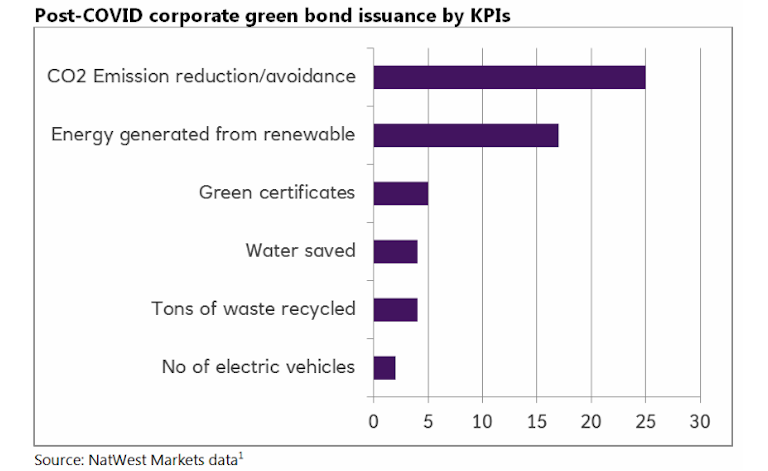

Post lockdown, one of the key questions is how the private sector is embracing a green recovery.

21 Jul 2020

. 3 min read

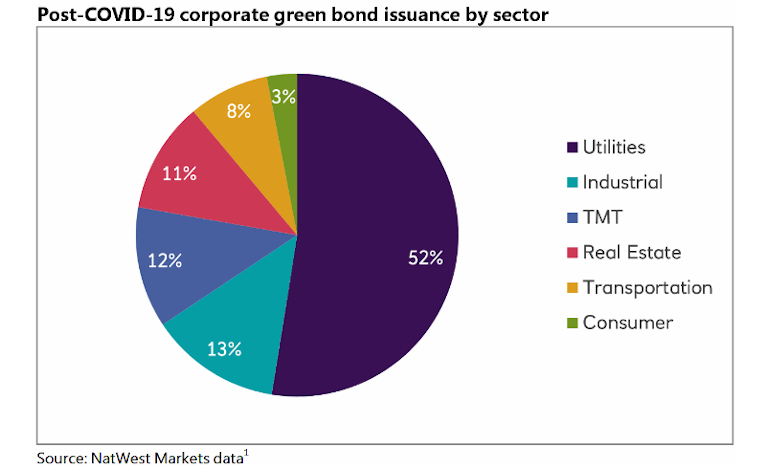

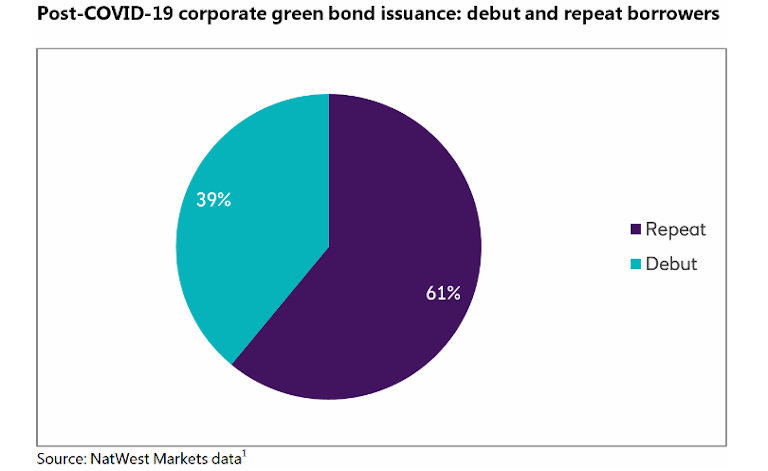

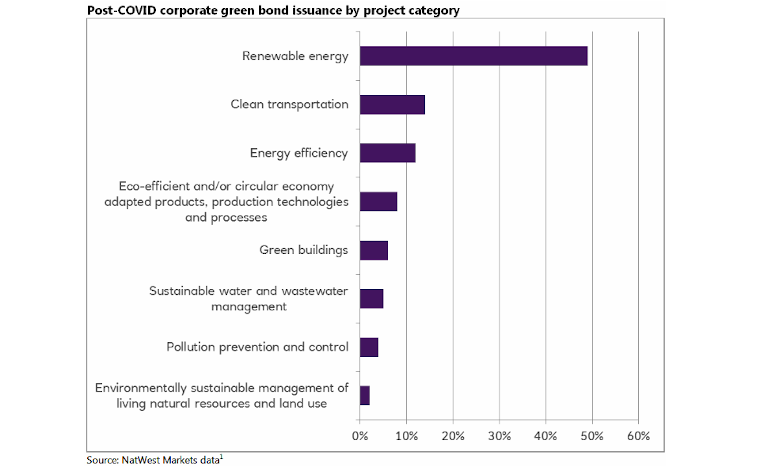

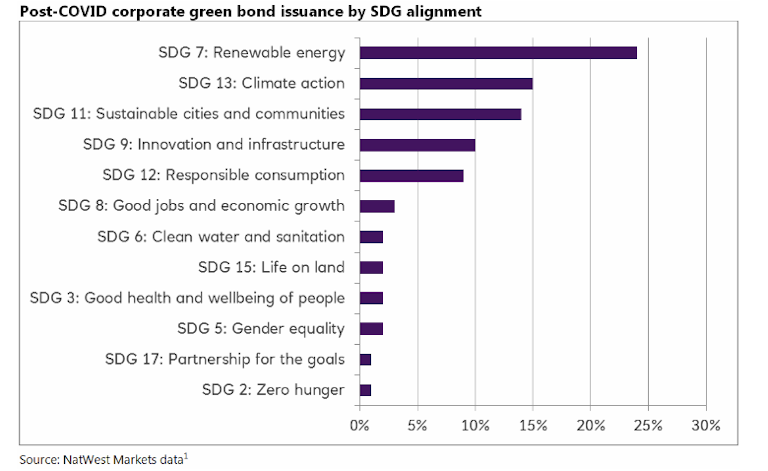

The green bond market, as the funding instrument of choice for large, environmentally focused corporates, may provide a useful perspective.