Sustainability

Going green for your maiden bond issue

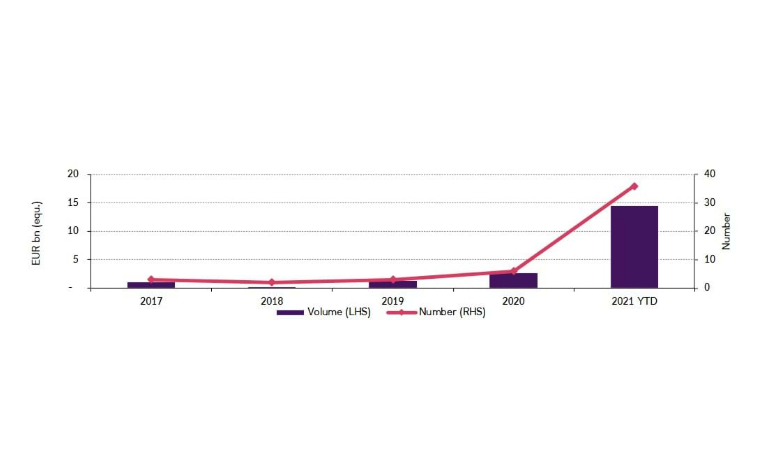

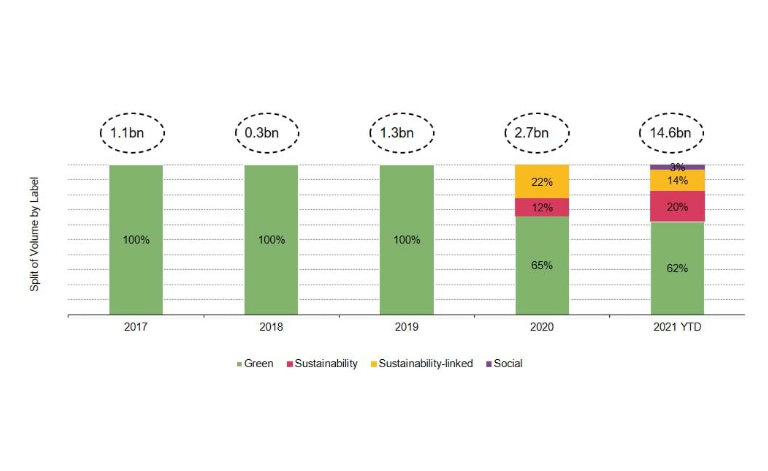

Want further evidence that green finance is becoming mainstream? Then look at the exponential increase of inaugural bond issuers opting for a sustainability label: in 2020, 6 issuers raised €2.7bn, while in 2021, year-to-date, 36 issuers raised €14.6bn sustainable debt.

18 Oct 2021

This is noteworthy. Conventional debt capital markets wisdom dictates that a first public fundraising should be a relatively “straightforward” proposition to the market, thereby not complicating matters for investors having to onboard a new credit.