Sustainability

Financial Institutions ESG Monthly – 11 March 2022

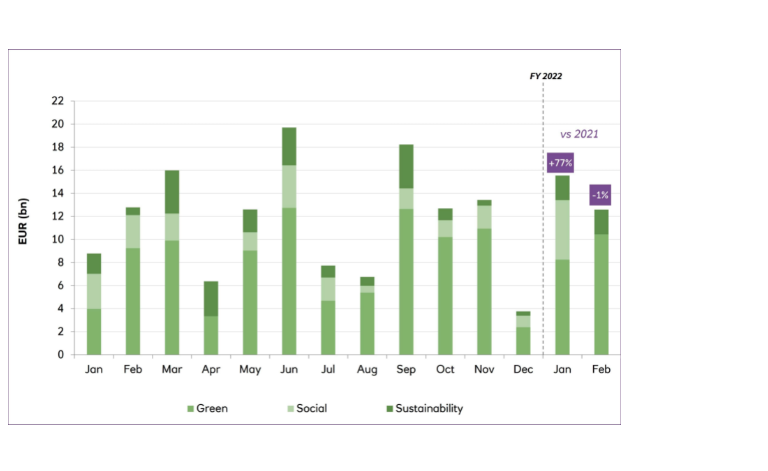

FI Green, Social and Sustainability (“GSS”) issuance was spread fairly evenly across the first three weeks of February. Thereafter, Russia’s invasion of Ukraine on the 24 Feb brought a sudden halt to further issuance activity.

11 Mar 2022

Since the invasion began, there has been a complete absence of FI issuance activity in the GSS market, despite us seeing some non-ESG issuance by FIs (particularly in USD).