Sustainability

ESG News: The sovereign effect on European sustainable debt issuance

When governments take the lead, others follow.

13 Jan 2021

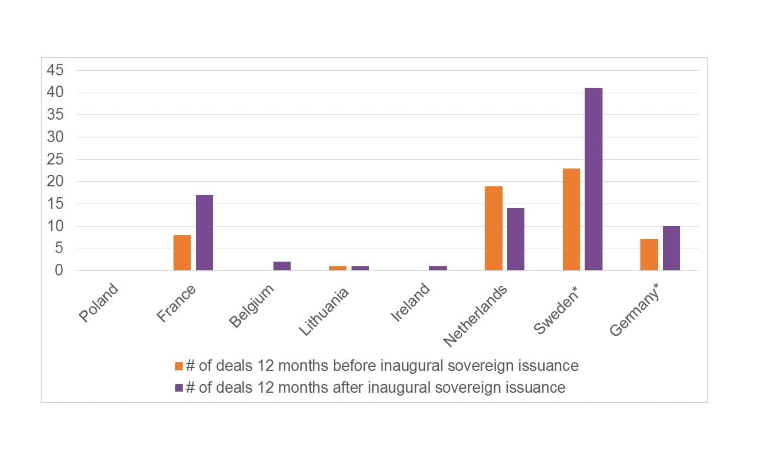

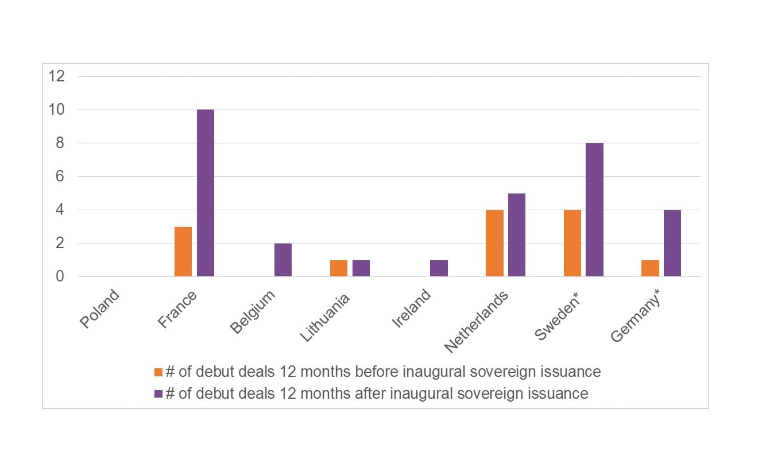

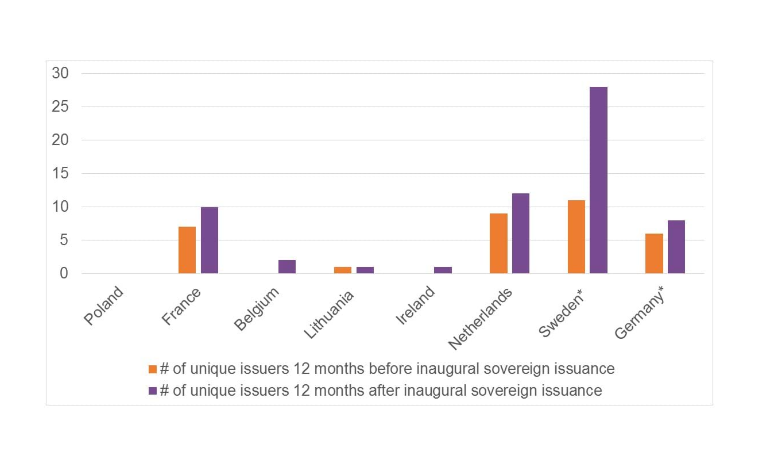

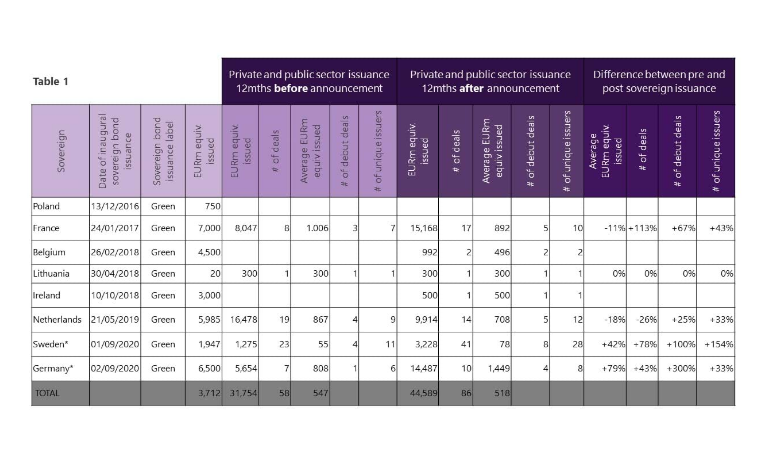

The recently-announced green gilt has raised hopes for broader growth in the UK sustainable corporate bond market, because sovereigns have shown themselves to have a “knock-on effect”: they clearly set an important example, have direct influence with their country’s corporates and, more broadly, can meaningfully increase available liquidity for sustainable debt through their issuance.