ESG investing has its foundations in investment strategies that excluded industries not aligned to religious values, and the divestment movements focused on college endowments in the 1970s and 1980s. It has now expanded to various strategies that consider ESG information as part of portfolio construction. Over the last two years, there has been an increase in inflows from both retail and institutional investors[1], driving a significant uptick in the number of funds available[2].

In order to differentiate their funds, asset managers have sometimes made unclear claims about the underlying investment process, use of ESG information, or the impact that investing in these funds actually has – with any of these actions to be considered as ‘greenwashing’. Environmentalist Jay Westerveld used the term greenwashing for the first time in 1986[3] while referring to the practice of making diverting sustainability claims to cover a questionable environmental record. For asset managers this means providing misleading information about how a fund or investment strategy are more environmentally friendly. The outcome from this increased assessment of manager claims may have a wider effect on the entire sustainable finance and investment ecosystem.

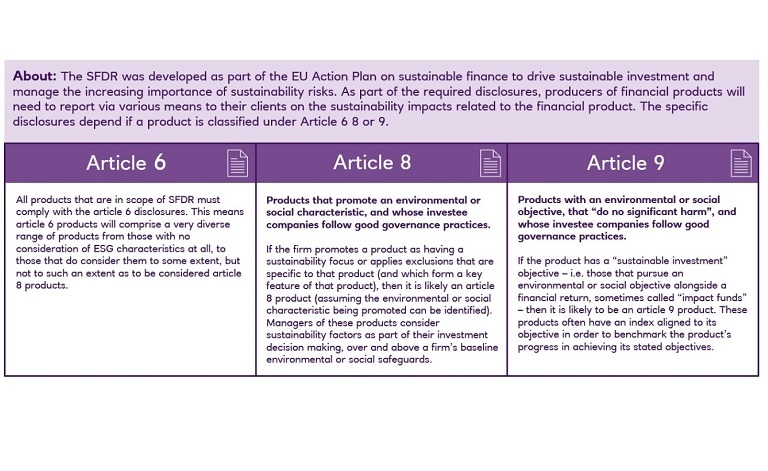

During this same period, attempts have been made to codify the disclosures around how asset managers use ESG information in the investment process, so that investors have the information they need. The most well-known of these is the EU’s Sustainable Finance Disclosure Regulation (SFDR), which requires asset managers to label all funds marketed in Europe according to one of three categories. The definitions for the labelling funds are not very clear, (but more granular criteria are coming)[4], and there are currently limited consequences for asset managers if they mis-label a fund or do not make the appropriate disclosures to support the labelling, as regulators allow for some bedding in time for asset managers to comply with the new rules. However, this is expected to change very soon.