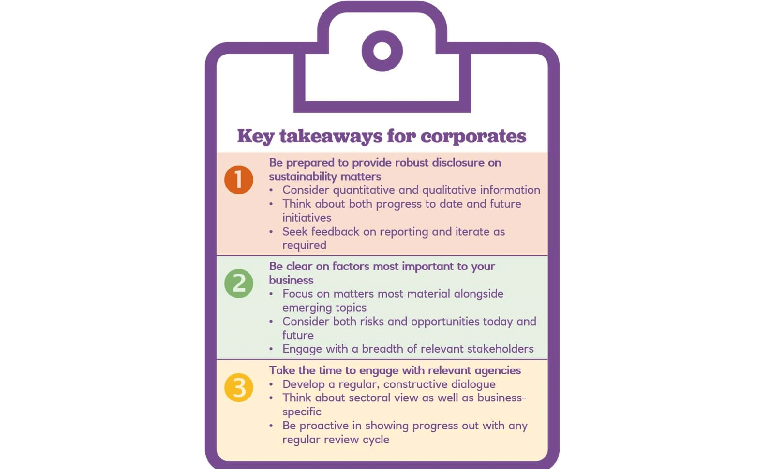

For issuers, ESG ratings can be an efficient means to communicate to investors and other stakeholders their ability to identify and manage ESG-related risks and opportunities. To ensure an accurate assessment of their ESG performance, issuers can also take a proactive approach to managing their ESG ratings to demonstrate improvement (e.g. change in ratings over the years) or to identify areas to focus on via peer benchmarking. Regardless of the use of ESG ratings, evaluating corporate performance on sustainability issues and then distilling that performance into a score or rating is an important part of the sustainability movement. These ESG ratings allow an accessible understanding of which companies are leading and which are lagging in a particular sector, and more generally.

The current lack of uniformity and opacity of ESG rating methodologies can lead to confusion for issuers when explaining their sustainability performance to their investors. It may also be difficult for issuers to explain why areas rated as strengths or weaknesses are perceived to be so by a particular ESG rating agency. Therefore, it is important for issuers to engage with a set of key rating agencies that are most relevant to their investor base, to be able to understand ‘why’ they received the rating they did, how to improve it – and crucially – to explain it.

Getting direct feedback from stakeholders can help inform which agencies issuers should engage. Issuers can use these discussions to make sure that information that they do want to be public is easily accessible and clearly labeled, with a strong rationale for why non-public ESG data is private or why it is not material to their business. That said, robust, reliable and regular disclosure – best published as part of annual reporting cycles – is the optimal method of ensuring strategic initiatives filter into ESG ratings. Of course, this disclosure should be material to the issuers and underpinned by action.

Efforts to gain a strong ESG rating should not be seen as a substitute to any efforts to improve sustainability performance, but rather as a way to describe current performance progress in managing material ESG-related risks and opportunities. Similarly, ESG ratings should also not be seen as a proxy for developing (and implementing) a credible sustainability strategy.

An ESG rating is a dynamic indictor, which can change over time based on evolving methodologies, and as a result it’s common for ratings to rise and fall. This is particularly true for a sector coming under transformative ESG pressures. With this in mind, in the same way issuers should engage with the ESG rating agencies to understand the ratings, they should also maintain a constructive dialogue with those relevant agencies to highlight strategic developments which could drive an improved assessment and help them to understand the intricacies of a particular business. A constructive dialogue can also aid issuers in understanding broader sectoral views held by investors.