Regardless of the type of sustainable debt structure used, the issuer is expected to have a framework that explains their sustainability financing approach, and how it links to the corporate’s overall strategy and sustainability objectives.

Whilst there is no legal requirement around these disclosures, there are plenty of voluntary guidelines for these frameworks and disclosures to align to. These guidelines, such as the ICMA Green Bond Principles or Sustainability-linked Bond Principles, explain the basic considerations that issuers should consider when selecting projects or KPIs, and the level of transparency that they should provide. For example, with a green bond, if proceeds can be used for re-financing, or the asset value approach is applied, then it is important that the issuer provides rationale on why re-financing is appropriate, and how the overall projects and eventual impact metrics feed into the sustainability strategy.

There is value for issuers to be transparent in pre-issuance disclosure on the ESG nature of the bond by covering details such as expected project split by types of project, geography or even expected impact. For green bonds in particular, investors may focus on what we coined, in a previous article, as the 4 As:

- Ambition: Is this business as usual, or is an issuer seeking to be industry leading in embracing the carbon transition?

- Alignment with the issuer's overall strategy: Is it a "side show" project, or truly congruent with a company's overall operations?

- Additiveness of the projects: What portion of proceeds will go towards new initiatives?

- Analysis offered on projects: What is the expected, measurable environmental impact?

With a sustainability-linked bond, to ensure that investors feel comfortable with the KPIs and targets, details on the selection of KPIs and the linkage to the issuer’s sustainability strategy should be clearly communicated along with sufficient information on why the targets go beyond what the company would achieve through “business-as-usual.”

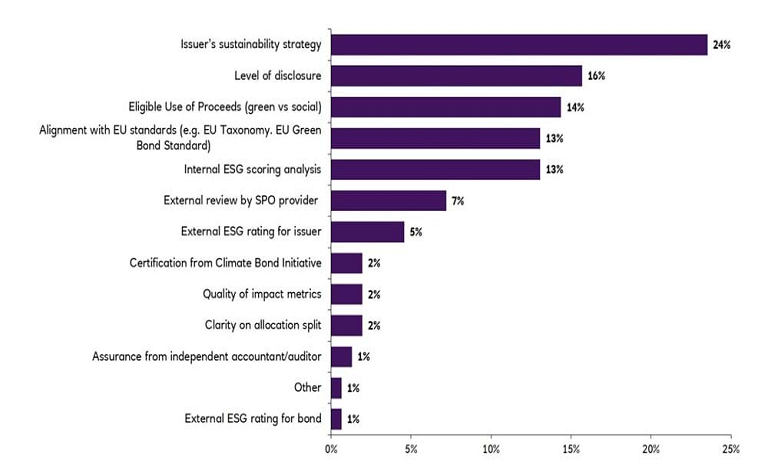

It has become market convention to obtain a “second-party opinion” (SPO) for Sustainability Finance Frameworks and their alignment to the relevant principles, such as the ICMA principles. However, as identified in our survey (Figure 2), only 7% of global investors considered the SPO to be among the top two most important factors when evaluating the robustness of Sustainability Finance Frameworks.

This may be because investors expect a positive opinion; therefore appointing an unknown provider or having a highly critical opinion can be unhelpful for issuers and cause undue focus on the negative aspects of the opinion. We expect it will become ever-more important for the disclosures on the issuances – and indeed the issuer – to clearly link the bonds’ KPIs or projects to the overall sustainability strategy. This also includes the post-issuance reporting: all GSSS bonds require regular reporting, which is a good opportunity for issuers to show that the targets or projects outlined in their Frameworks have been met or implemented (or are on track to be), and that those projects or KPIs are still relevant to the sustainability objectives. Beyond simply showing progress against KPIs or that funds have been allocated appropriately, it’s equally important to show investors that these financing instruments continue to help deliver the company’s overall sustainability strategy.