Sustainability

Decarbonisation on the menu: Is the food industry being adequately incentivised to achieve net-zero?

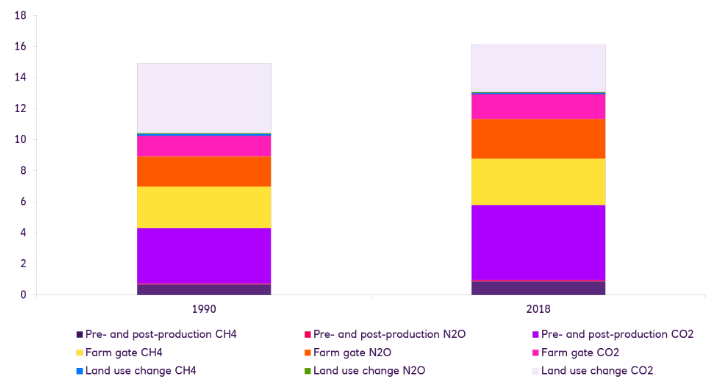

Food production is altering the trajectory of net-zero: the industry generates as much as 40% of global greenhouse gases – but investing in innovation to improve yields and energy efficiency, and reduce waste, can help.

01 Feb 2022

Emissions intensity has not influenced investment into the food production sector: we couldn’t find a strong link between investment flows and stock market performance – meaning climate risk isn’t being priced into assets.