Having surveyed various FIs earlier this year, it’s fair to say that the organisations were at very different stages of their journey. While some said they are still learning about how to effectively measure and monitor all three scopes of emissions, others told us they are considering a public net-zero target pledge with definite deadlines. Another group of FIs mentioned that they are looking at how carbon offsets could be used to supplement their portfolios and support their organisation’s wider objectives to reduce residual risks, or how the purchase of carbon credits could help protect natural habitats and biodiversity.

Key take-aways included:

- It starts with the right metrics: there’s a lot of work underway at the moment to get the data/metrics in place that help measure the emissions in the first place; not a simple or straightforward task as pointed out by many.

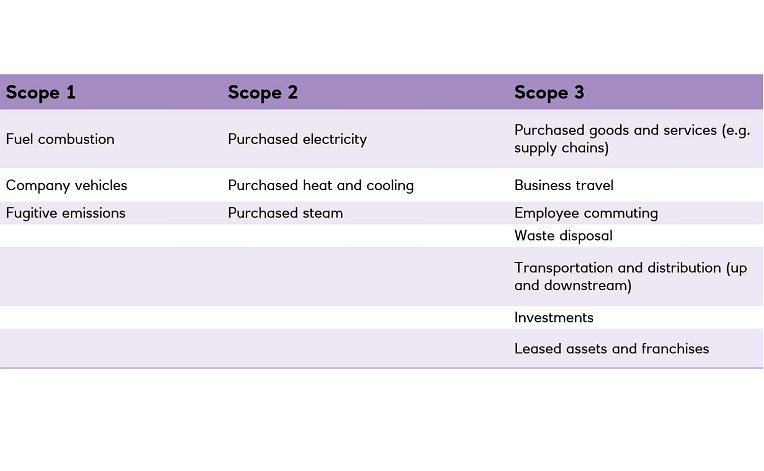

- Carbon credits in demand: FIs have been using a wide range of carbon credits over the years, particularly for their own operational emissions (scopes 1 & 2), but increasingly also for scope 3 emissions; alongside switching to renewable sources. With an increasing number of FIs considering offsets, there is potential that the costs for offsets will increase.

- Who’s to pay: there’s an ongoing discussion about who should pay for the offsets e.g. the asset manager or the asset owner?

- Inclusion of carbon credit in emission targets: there are divergent views when it comes to the question of allowing carbon credits to be used to achieve emission targets. Organisations, who have signed up to the Science Based Target Initiative (SBTi), are not allowed, by definition, to use offsets, although offsets are still considered valuable for the residual carbon footprint. By contrast, the Net Zero Asset Managers’ (NZAM) Initiative allows for offsets if there is no financially or technologically viable alternative.

- Divestments not a quick solution: selling off high emitting assets may not be the answer to support the transition to net-zero or to achieve systemic change.

Looking more closely at different categories of FIs, this is what we’ve heard from each group:

Banks

- Active support for carbon credits: some banks already apply or strongly support the generation of carbon credits. The credits are bespoke in nature or for their own bank offsetting initiatives. In particular banks with public net-zero commitments are using carbon credits. However, banks have not applied carbon offsets to the carbon emissions (scope 3) of their loan portfolios.

- Net-zero not universal: not all banks have net-zero ambitions. Instead, they have set themselves % targets for certain dates; often applying different targets and timelines to the different scopes.

- Disclosures vary substantially: mainly depending on bank size, disclosures range from full emission breakdown per scope to no disclosure whatsoever for some of the smaller/start-up banks.

- Building societies vary in approach: while some use carbon offsets already, others make no mention of their emissions or targets in their published reports.

Asset managers

- Net-zero funds: in the last three years, an increasing number of asset managers have launched funds targeting net-zero investment options.

- Verifying offsets: different asset managers are using different sources for their offsets and different ways of verifying them. Verified Carbon Standard (VCS) and Gold Standard were the most frequently mentioned.

- Only a minority of asset managers are currently willing to buy carbon credits: while a few asset managers have agreed to buy and absorb the costs of carbon credits for specific portfolios, this clearly was the minority of those we surveyed. However, some are open to discussing carbon credits but are not yet set-up to do so at a portfolio level. We also heard asset owners have not (yet) fully embraced carbon credits.

- Seeking dialogue about net-zero: many portfolio managers told us they are keen to continue engaging with the underlying companies to promote emission reductions rather than those companies relying on carbon credits.

- Emissions matter: if all else is equal, portfolio managers are likely to choose the lower emitting company over a higher emitting company if all other metrics are similar (and available), emphasising how ESG data is affecting portfolio management and investment decisions.

Pension Funds

- Feeling the pressure: apart from regulatory pressure, pension funds are also increasingly challenged by organisations such as MakeMyMoneyMatter[4] to consider public net-zero targets. As a result, some are discussing carbon credits as an option with their asset managers, albeit it will likely be the asset manager that buys and holds the carbon credit on the pension fund’s behalf.

- Carbon offsets and fiduciary duty: there are questions around the appropriateness for pension funds to use carbon offsets given their fiduciary duty (and when the offset itself does not explicitly provide an expected return but incurs a cost, thereby reducing the return). Others argued that if carbon credits rose in value then they could be sold in the future as a net gain. Some however, were open to the idea of using carbon offsets (albeit described as ‘early stage’ thinking), if it could help them meet their net-zero target or impact objectives.

- Data and disclosures: similar to other FIs, many funds are still working on getting emission data right as well as their disclosures – for example aligning them with the Task Force on Climate-Related Financial Disclosures per the recent regulations.

What’s next?

Carbon credits are not a new concept although are arguably gaining more attention as more entities adopt net-zero targets and are looking at portfolio emissions and ways to reduce them – as well as the growing focus on establishing robust infrastructures to reduce some of the unknowns. Carbon credits are seen by many as a ‘last resort’ but a useful step nonetheless in helping to sequester carbon from the atmosphere. With prices set to increase, if much of the increased demand expected from FIs does start feeding through into carbon credit pricing, questions around when the right time is, the extent to which FIs engage and the technology which they use to do that, could well dominate agendas.

Follow our Carbonomics 101 series, where we address these questions (and more), to help you stay informed on the development of the carbon markets and learn about the role they play in achieving net-zero. For our next instalment we will be taking a look at what the voluntary carbon markets mean for Corporates.

*NatWest achieved Net Zero Carbon across its operations in 2020. We achieved this through a combination of emissions reductions, alongside offsetting residual Scope 1, 2 and 3 emissions (business travel) through the purchase of internationally recognised TIST (The International Small Group and Tree Planting Program) Carbon Credits.