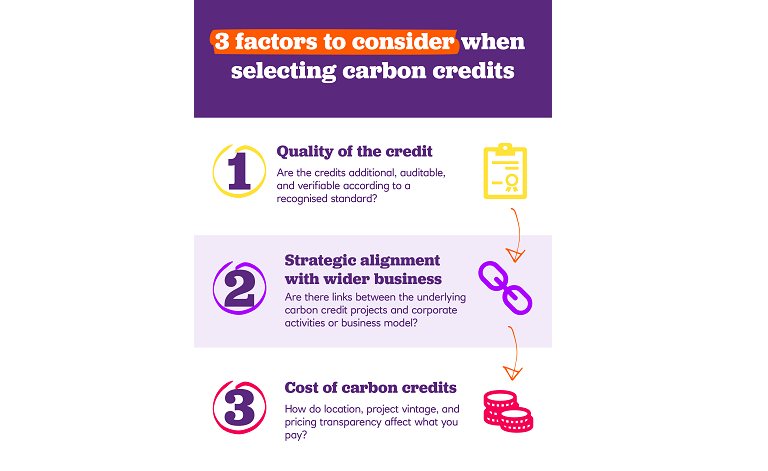

While there are many factors that can determine the choice of carbon credit, we focus on the three most important ones for corporate decision-makers.

1. Quality of the credit

Needless to say, carbon credit quality is quintessential. The integrity of the carbon offsetting concept relies wholly on the environmental additionality of the credit, which all standards (which we outline later in this article) define in the same way: a carbon credit is considered additional if the emissions reduction/removal that underpins the credit would not have occurred without the project that generates the credit.

While this might sound obvious, there have been issues with poor-quality, legacy credits, where projects offering credits would have happened anyway without the additional funding from the credits. In these cases, buying the credits didn’t result in additional reduction/removal of carbon from the atmosphere, meaning the carbon credits of these projects generated no environmental benefit.

Standards are key and have been developed to ensure that credits offered on global carbon credit markets are genuinely additional, auditable, and verifiable. While very similar in their approach, these standards differ depending on the type of carbon credit – of which there are two.

Certified carbon allowances are traded in compliance carbon markets. These are applied to the power, heat generation, oil refineries and commercial aviation industries, representing the regulated ‘stick’ that puts a price on GHG emissions. It’s commonly known as the UK Emissions Trading Scheme (ETS), where companies buy emissions ‘allowances’ at auction. These don’t actually remove any GHGs from the atmosphere, whereas carbon credits do.

Voluntary carbon credits are traded on voluntary carbon markets, which function outside but in parallel of the compliance market. Voluntary markets operate not because of government obligations but to give companies and others the opportunity to offset their own emissions on a voluntary basis. Carbon credits can be created under voluntary market standards, the most notable of which are:

- Verified Carbon Standard (VCS): Developed by VERRA, the VCS standard provides real, quantifiable, additional, and permanent projects-based emission reductions. Credits are managed through registries to register, transfer, and retire Voluntary Carbon Units (VCUs).

- Gold Standard Verified Emissions Reduction (GS VER): Launched in May 2006 by the World Wildlife Foundation, the GS VER is only available for projects in developing countries with a focus on renewable energy and energy efficient projects with strong sustainable development benefits.

- Voluntary Offset Standard (VOS): The VOS is based on standards promoted by the United Nations Framework Convention on Climate Change (UNFCCC), and as such brings the voluntary market on to the level of the certified carbon credits markets.

- Climate, Community and Biodiversity Standards (CCB): Developed by the Climate Community and Biodiversity Alliance, this standard is for land-based projects that can deliver climate biodiversity and community benefits simultaneously. The CCB uses methodologies of the Intergovernmental Panel On Climate Change (IPCC) ‘Good practice Guidance’.

- UK Woodland Carbon Code (WCC): The WCC is the quality assurance standard for woodland creation projects in the UK. It is internationally recognised for high standards of sustainable forest management and carbon management and is endorsed by the International Carbon Reduction and Offset Alliance (ICROA).

Standards are becoming stronger and increasingly multi-layered as more organisations get involved in their development. A good example of this is the Core Carbon Principles (CCP), a new internationally recognised standard for global voluntary carbon markets developed by the Taskforce on Scaling Voluntary Carbon Markets (TSVCM). The CCP sits alongside a range of other frameworks, legal principles and contracts developed by the TSVCM providing better governance, transparency, and scalability in global voluntary carbon markets.

2. Strategic alignment with the wider business

Choosing carbon credits with strong links to an underlying business model and corporate activities can help make emitting activities more aligned with emissions removal, which is desirable from the standpoint of a wide range of external stakeholders – lenders, investors, and regulators included. After assessing the quality of available carbon credits, applying a strategic and geographical/supply chain lens to gage alignment between credits and business activities will help produce a "carbon credit short list".

In doing so, companies and organisations should ask themselves the following questions:

- Are there links between the underlying projects of the identified carbon credits and the core business model?

- Do the carbon removal / avoidance activities of those projects align with the company’s emitting activities?

- Are those carbon credit projects based in countries where corporate activities (suppliers) are causing emissions to rise?

- Are the projects having a positive impact on local community and biodiversity near operations?

Intermediaries can also support in finding projects that fit strategically with the credit buyer’s business.

3. Costs of carbon credits

Finally, comparing the costs of carbon credits of equal quality and equal fit with the business is the natural next step to finalise the choice of suitable carbon credits. However, the pricing of carbon credits remains very elusive, mostly because of the wide variety of credits in the market and the number of factors influencing the price. Credits can currently cost anything from as low as $3 to $200 per tonne depending on a range of factors, with many estimates forecasting price increases over the next few years.

One of the main factors affecting the price of carbon credits is the nature of their underlying project. Projects are grouped into two large categories or baskets:

- Avoidance projects, which avoid emitting GHGs completely, reducing the volume of GHGs emitted into the atmosphere. These include off-grid renewable energy projects, projects to prevent deforestation and farming emission reduction projects, and the development of energy-efficient buildings.

- Removal projects, which remove GHGs directly from the atmosphere. These include nature-based projects (for instance, using trees or soil to remove and capture carbon) and tech-based projects (such as human-made carbon capture and sequestration).

Removal credits tend to trade at a premium to avoidance credits, not just because of the higher level of investment required by the underlying project, but because of the high demand for this type of credits. They are also believed to be a more powerful tool in the fight against climate change because no carbon would have been removed without the project. With avoidance (or reduction) credits, it is less clear what would happen without a particular project. Beyond the type of the underlying project, the price of a carbon credit is also influenced by a number of other factors which we outlined in a previous article of our Carbonomics 101 series.