Increasing evidence has highlighted risks from nature loss over the coming decades. c.50% of global GDP is moderately or highly dependent on nature and its services[1]. This creates material risks and opportunities for financial institutions, asset owners and asset managers, as they lend or invest in companies facing increasing threats associated with biodiversity loss. However, the world’s ecosystems have already diminished by 47% globally, relative to the earliest estimates, with 1 million species at risk of extinction. Therefore, this is not just a financial consideration but survival.

The United Nations (UN) Biodiversity Summit has been delayed due to COVID-19 and is currently expected to take place in October 2021 in China, ahead of COP26. This conference aims to have countries agree to a global biodiversity framework with internationally binding targets for biodiversity (akin to the 2˚C of the Paris Agreement for climate) providing a guiding light for all market participants. It is proposed that milestones by 2030 will be interim steppingstones for 2050 goals, including increasing the area of natural ecosystems by at least 5% globally and halving the number of new introductions of invasive species globally[2].

Whilst at a supranational level, work is still being done to establish ‘value’ and agree targets for biodiversity, it is arguably a slower process to integrate this into financing efforts. At present, many projects that damage biodiversity are not explicitly punished, nor conservation of biodiversity explicitly rewarded. The emergence of KPI-linked products for a number of asset classes continues to rise, with this being one area that could be considered. Whilst climate measurability is challenging, biodiversity is even more complex given the interconnectivity and far-reaching impact. It is not surprising perhaps that disclosure and reporting around biodiversity has not been as high on the agenda as climate change metrics, such as emissions, but there is growing recognition that this is an area of material importance.

Whilst the Task Force on Climate-related Financial Disclosures (TCFD) is increasingly used by many asset owners, managers and corporates to report climate-related intent and purpose, the newer Working Group for the Task Force on Nature-related Financial Disclosures (TNFD) created last year and formally launched last week, is hoping to be embraced as the equivalent for natural capital. The current thinking includes a 'double materiality' approach[3] i.e. both how nature impacts a company and its operations, in addition to how the operations of a company impact nature. However, more work is needed to distil this into straightforward measures that financial market participants can track, monitor and report.

As Barbara Pompili, France's Minister of the Ecological Transition, said: "The challenge of biodiversity and nature preservation is crucial. We need corporate and financial institutions to take their parts. Yet, we lack unified definitions, standards and metrics to accurately and thoroughly embrace nature preservation. The TNFD will constitute an important step to start properly addressing at [the] global level biodiversity-related risks and impacts."[4]

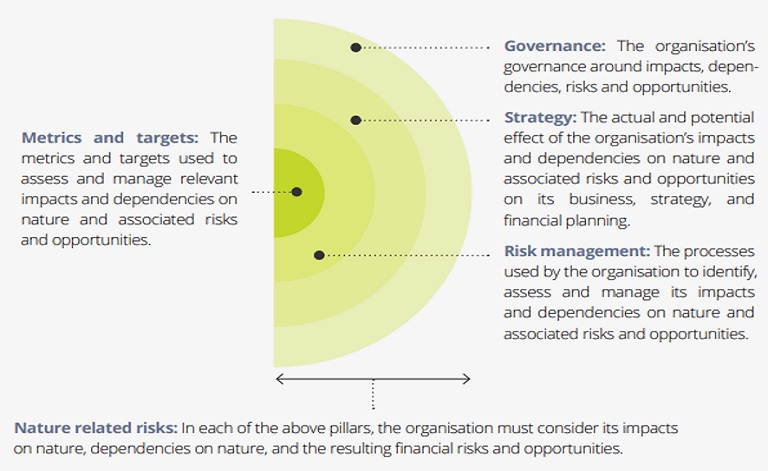

The TNFD, like TCFD, will use a four-pillar approach (governance, strategy, risk management and metrics & targets), shown below. By 2023, they will deliver a framework to report on nature-related risks to shift financial flows towards ‘nature-positive outcomes’ and/or reduce the ‘nature-negative outcomes’: