In January 2022, the EBA published the final standard on prudential (Pillar 3) disclosures that will require the ~150 largest banks in the EU to begin reporting on their ESG risks and sustainable finance strategy, mostly starting from 2024.

The disclosure rules will initially focus on Climate Risk (and would need Quantitative Information) with a view to extending the scope to cover other environmental risks when the EU Green Taxonomy is complete. Qualitative Information is required around Social and Governance risks.

The requirements set out by the EBA for bank disclosures dovetail into those above for the Taxonomy Regulation, and more generally the recommendations made by the Task Force on Climate-Related Financial Disclosures (TCFD). But they also go further in asking institutions to identify exposures that highly contribute to climate change. Per the technical standards, disclosures will include:

- Qualitative disclosures on ESG risks

- Quantitative disclosures on climate change transition risk

- Quantitative disclosures on climate change physical risk

- Quantitative information on KPIs including green asset ratio (GAR) and banking book taxonomy alignment (BTAR)

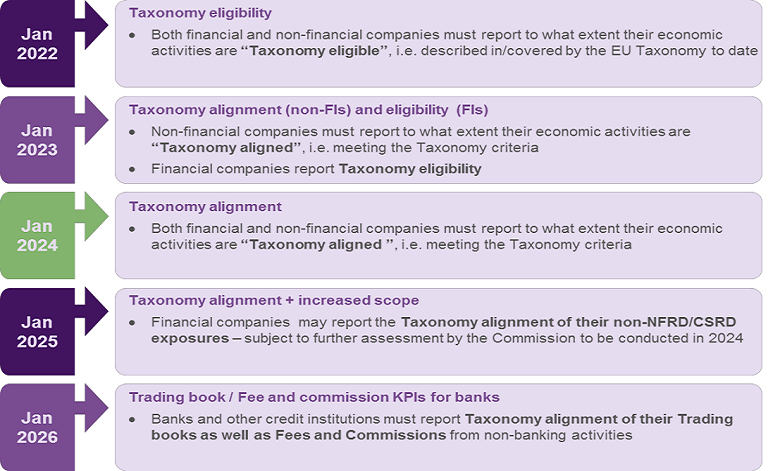

In terms of when, some level of disclosure under Pillar 3 will come into play in 2023 (for period 2022) but the bulk of disclosures will apply from 2024 (by which time banks in theory will have a year’s worth of taxonomy-alignment data from non-financial corporates).

There is clearly risk here – banks will be expected to present quite granular data on the ESG risks associated with the exposures they hold, but that data will be highly dependent upon the quality of data a very wide range of counterparties will be supplying to them. In the absence of such data, banks may need to consider reasonable proxies by sector or geography, with the legal and reputational risks that might entail.