What next?

Per the £RFR roadmap, the key upcoming milestones are:

· Q1 2021: no new £ LIBOR loans and no new linear £ LIBOR derivatives (except for risk management of existing positions)

· Q2 2021: no new £ LIBOR non-linear derivatives (same exception)

· Q2-Q3 2021: cease cross-currency swaps referencing £ LIBOR

· Q3 2021: complete active transition of legacy £ LIBOR exposure where viable

· Q4 2021: no new USD LIBOR derivatives (ARRC8 milestone, similar hedging exception to GBP)

In February 2021 we saw the RFR Working Group (WG) make a further announcement concerning the Q1 linear derivative deadline providing some clarification, but emphasising that “the intention is for continued use of GBP LIBOR via risk management exceptions to be kept to a prudent minimum”.

Of course the ‘turning off the tap’ milestones are one thing; it’s clear now that the path is set, increasingly the focus will turn to active transition. The WG has set a target of Q3 to complete all active transition for LIBOR cash & derivatives “where viable”.

We’ve seen the RFR Credit Adjustment Spread paper in December and the Best Practice Guide for GBP Loans in February aimed at helping the loan market, and we may see more from the WG soon on the operational considerations of transition using fallbacks. But there are naturally some in the market that won’t wish to actively transition and would prefer to rely on fallbacks to do the hard work for them, notwithstanding those operational challenges.

What about cleared swaps?

While the market waits on final plans from LCH9 for mass conversion of outstanding LIBOR trades shortly prior to the relevant LIBOR cessation date, the preliminary results suggest LCH will move away from cash compensation for the basis spread and will instead incorporate the basis into the new RFR leg. Further details to follow around precise conversion mechanics and timings. LCH has also confirmed that any transition of USD would happen at a later date.

Final thoughts

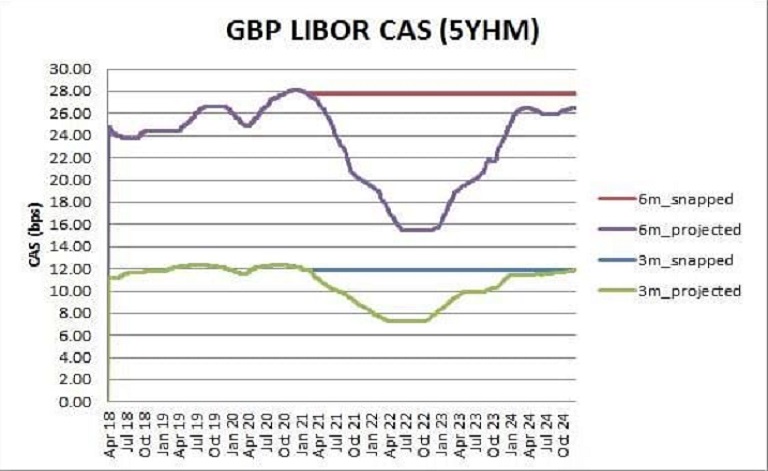

With this announcement fixing X, the widespread adoption of fallbacks, an emerging solution for non-linear referencing ICE Swap Rate, and some explicit ‘no new trading’ milestones, the path for derivatives is becoming fairly clear. With $ cessation confirmed as June 2023, also expect to see some pick up in RFR based x-ccy trades as SOFR liquidity develops.

The one remaining unknown is the speed at which active transition of legacy derivative portfolios will occur. Regulators are keen to see this happen, but many derivatives may hedge legacy loans or bonds that are still on LIBOR, and so hedges will only move at the pace of those transitions. And even beyond that, do counterparties want to actively move derivatives, or would they prefer to wait for fallbacks?

We will see whether now the uncertainty on X is gone, active transition accelerates. X may mark the spot, but it doesn’t mark the end.