However, the US market has become much more vocal on this topic recently. The ARRC released conventions papers in August and November, and the New York Federal Reserve has launched a consultation on publishing SOFR compound averages and an index on their website.

Most recently, an ARRC loans sub-working group is reviewing alternative compounding approaches in order to address requirements of the secondary loan trading market in relation to interest allocation and provide loan platform providers with clear methodologies to code into their systems – expect a recommendation from the working group to the ARRC early in the new year.

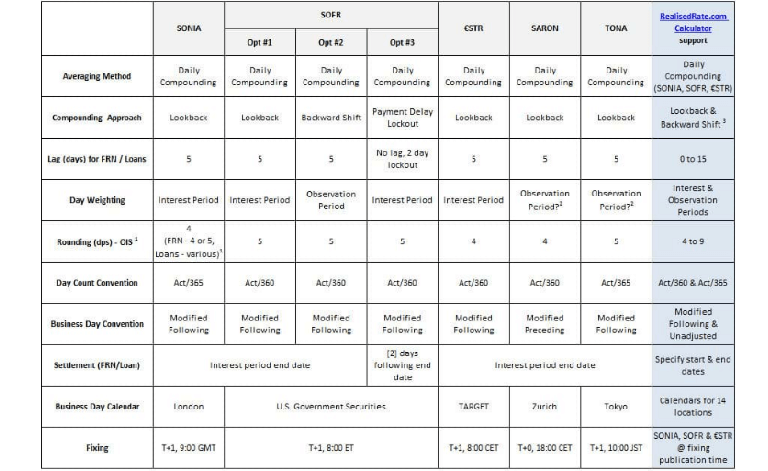

The latest ARRC paper lists three models for SOFR FRNs using the Daily Compounding method:

- Lookback - same as the SONIA standard for FRNs and Loans, with [5] day lag of the daily rate to the earlier Observation Period but with day weighting remaining against the Interest Period

- Observation Period Shift- 'Backward-shifted' model where both rate and day weighting shifts back to the earlier 'Observation Period'

- Payment Delay- in ARRC paper this option includes both a Payment Delay (eg settlement 2 days after Interest End Date) and a Lockout (daily rate 'suspended' for final [2] days of interest period, referred to as 'Rate Cut-off Date'); note in FSB paper these options are presented separately

The "weight" refers to the weighting in the compounding formula to account for calendar days when the RFR is not published (e.g. at weekends).

Outside of the averaging approach, other details also vary between benchmarks...SONIA and euro short-term rate (€STR) derivatives round to 4 decimal places by default, whereas SOFR rounds to 5 dps. SOFR and €STR use an Actual/360 day count convention, whereas SONIA uses Actual/365. These are well known defaults within the international swaps markets, but may not be so familiar across the wider industry. See the table below for a comparison of conventions.