The battle of conventions - 'shift v lag'

As we set out in Compounding the problem with conventional wisdom? last November, one of the key challenges in adoption of RFRs is agreeing which conventions to use. The publication of an index, particularly if BoE and NY Fed agree to calculate each in the same way, does help with settling some of these questions.

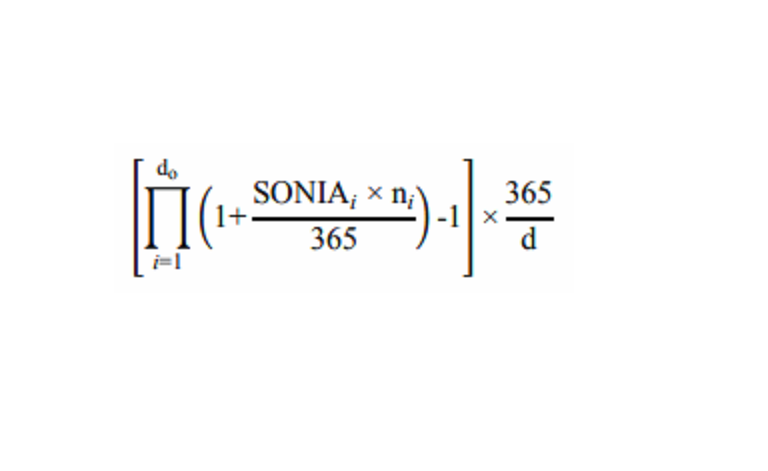

One area we pointed out where US and UK seemed to be diverging was on how the day weighting was calculated in the compounding formula when there is an offset between the reference period for the rates and the interest period.

UK had settled on the 'observation lag' approach (aka 'Lookback') in earlier SONIA Floating Rate Note (FRN) loans, however in US the Alternative Reference Rates Committee (ARRC) seemed to be leaning more towards the 'observation shift' method (aka 'Backward Shift'). The production of an index works best using the observation shift method, where the day weighting is aligned to the reference period.

The European Bank for Reconstruction and Development (EBRD) announced a new SONIA issuance last week that also adopted the observation shift convention. So with UK regulator now coming out with an index as well, it seems likely that 'shift' will win the day.

SONIA period averages

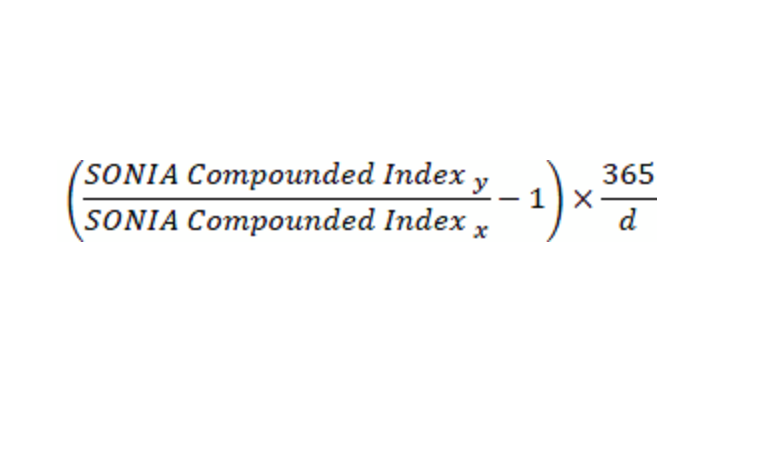

The BoE is also consulting on publishing what it refers to as 'SONIA Period Averages'. These will be compounded rates for standard periods like 3m, 6m and 12m, and equivalent to the 'SOFR Averages' that the Fed will publish. On RealisedRate.com we have standard tenor tables which do the same thing. In theory these can further simplify matters by publishing the standard 3m in arrears compounded rate on any given day.

The difficulty, as the BoE paper sets out well, is how you actually work out the start date for each period in a situation where three different start dates might legitimately be said to cover the same period due to the 'modified following' rule around business days at the period end. The paper suggests 3 options to define the reference period, one of which matches the SOFR method. If the BoE can't get consensus on the best methodology they may drop the idea to publish the period averages.

'Compound the rate' or 'compound the balance'

Another conventions face off that is currently in play is the discussion in the loan market between the relative merits of 'compound the rate' v 'compound the balance'.

This matters in loan agreements where the principal can fluctuate during the accrual period, and how this is handled across multiple lenders. This is a topic being discussed at loan working groups in both US and UK at the moment.

'Compound the rate' requires accrued interest to be repaid at any principal prepayment (or 'paydown') event whereas 'Compound the balance' does not, applying daily effective rate to principal and accumulated unpaid interest.

The industry appears to be moving towards the 'Compound the rate' methodology as it better aligns to publication of an index, but time is running out to agree methodology across the market and then get infrastructure providers to implement the solution in their systems.

And the stick....haircuts on collateral

The other thing announced by Andrew Hauser on Wednesday, 26th February is that there will be progressively higher haircuts applied to any London Interbank Offered Rate (LIBOR) linked collateral (maturing after 2021) posted with the BoE, rising from 10% in October 2020 to 100% by end of 2021. Also all securities referencing LIBOR (including loans) issued after 1 October 2020 will be ineligible.

This is to discourage the holding and use of such assets, as well as to apply a risk weighting to collateral that may become less liquid as cessation approaches. We would expect these steps to accelerate the sell down of LIBOR based FRNs and for issuers to step up consent solicitation for transition to RFRs (or inclusion of fallbacks).

The BoE consulted on this approach back in October last year, and it was largely anticipated that measures such as this would be put in place. There was a brief mention of sharper sticks that might be used to prod the industry in times to come should the stock of LIBOR not diminish (see Dec FPC summary), but no details as yet.

More Dakar than Grand Prix?

Perhaps the turbo charged racing analogy in the BoE speech is a little optimistic, but these are useful steps in the long road to cessation. Still more Dakar Rally than Grand Prix we suspect.

Phil Lloyd, Head of Market Structure & Regulatory Customer Engagement.