What are different client bases doing?

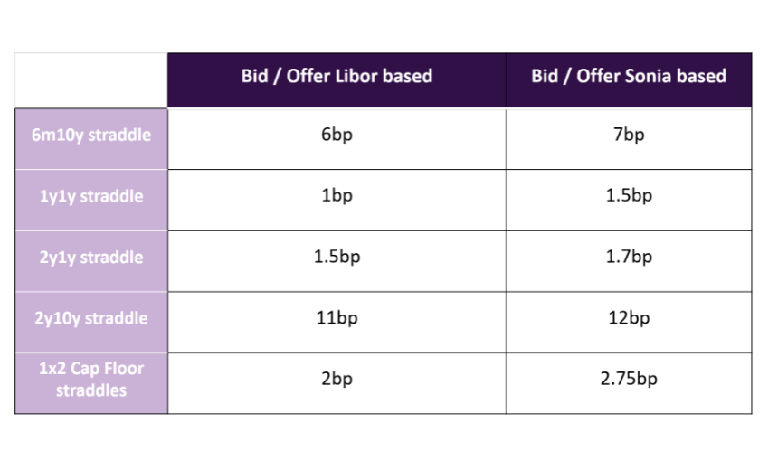

Real Money: We have started to see the first signs of Real Money clients moving towards trading SONIA Swaptions in 2021. Given the trading we have seen, and the bid/offer spreads shown, these participants appear to be getting good liquidity overall. From our conversations with clients yet to move, there is plenty of appetite for the move to SONIA as soon as feasibly possible. Q2/Q3 cited as expected timeline in accordance with market guidelines and has been noted that investors looking to trade expiries going over the 2021 year end will aim to do in SONIA format (or LIBOR initially with a view to rolling into SONIA later in the year).

Hedge Funds: A few inquiries, but Hedge Funds focused on liquidity as paramount. There is a definite willingness to move, but they will likely let the market lead and follow when liquidity is like for like (confirmation of fall back spread should be a big kicker here).

LDI8: Over the past few years we have seen a distinct shift away from using options from LDI. With the end of LIBOR on the horizon and typical expiries of LDI tending to be longer dated we saw a lot of these positions being transitioned into Sonia swaps. So far in 2021 we have seen a large increase in conversations, with accounts becoming quickly aware that relying on fallbacks might not be applicable to the volatility strategies they run. We have seen interest to transition existing collar positions as well as to look to enter into new trades now that pricing costs between LIBOR and SONIA Options have quickly converged.

Corporates and Banks & Building Societies: Active in SONIA Caps Floors towards the end of last year and the start of this year. Suspect this will be an ongoing theme throughout this year.

And how do we deal with legacy?

Lots of focus on the ISDA9 protocol and fallbacks. As we wrote about before, this path may not work for the wider non-linear market.

Swaptions: The Non Linear RFR Working group has been working on a formula that will create an alternative LIBOR Swap fixing using the SONIA Swap fixings and the yet to be published fallback credit spread. We are optimistic that this will be published in the coming weeks. The formula can be used to settled Legacy Cash Settled Swaptions & CMS10 contracts but the replacement of the LIBOR Swap Fixing with the alternative LIBOR Swap Fixing will not be automatic. Some form of market wide amendment is required to shift existing LIBOR Swap Fixing contracts to the alternative method. ISDA & the Non Linear task force are working on this.

Legacy Caps Floors: The fallback will represent a significant change in valuations with the optionality changing as detailed above as the contracts move from fixing in advance at the start of the coupon period, to fixing in at the end of the coupon period versus compounded daily SONIA. There will also be a two day fixing lag applied to legacy contracts. The market is well aware of these changes & has repriced accordingly

Other more exotic products can significantly change through fallback. These have been rarely traded so we won't go into them at length but details are given on the BOE document for non-linear transition and on the ISDA fallback statement.

Anything else?

LCH conversion process for LIBOR trades to SONIA was recently consulted on. We are concerned regarding Swaptions that expire between the planned date for this LCH conversion process & actual LIBOR cessation. Physically settled LIBOR Swaptions would be unable to settle into the LCH. The fallback states these would be Cash settled. Cash settlement of these and standard Cash settled swaptions will likely be impossible as with the LCH no longer accepting LIBOR swaps the LIBOR ICE fixing will fail.

Watch this space

We expect the LIBOR cessation announcement fixing the spread adjustment any day now. Question is what will this mean for the non-linear market? Are we ready to see this market really take off? Happy to have that conversation since we’re ready to go.

Phil Lloyd, NWM Sales

Christopher Michael, NWM Sales

Please click here to find all of NatWest Markets’ Strategy and Sales commentary/ideas.

You can also find out more about our electronic offering and credentials for Rates here and for FX here.

[1] LIBOR - London Inter-Bank Offered Rate

[2] RFR - Risk-Free Rate

[3] SONIA - Sterling Overnight Index Average

[4] FCA - Financial Conduct Authority

[5] ICE - Intercontinental Exchange

[6] IRR - Internal Rate of Return

[7] IPV - Independent Price Verification

[8] LDI - Liability Driven Investment

[9] ISDA - International Swaps and Derivatives Association

[10] CMS - Constant Maturity Swaps