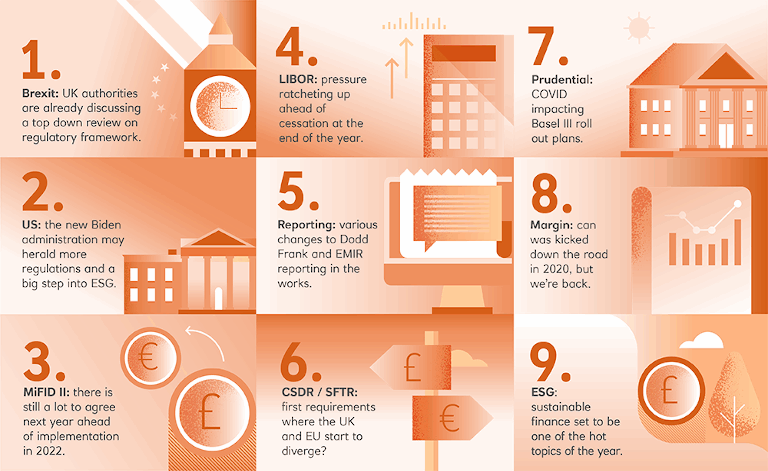

Key takeaway: we start with the same rules as the EU, but UK authorities are already discussing a top-down review of the regulatory framework.

There’s been a top-down consultation concerning the UK’s regulatory framework ahead of a review of, and recommendation of changes to, individual regulations. The focus has been on the principles that should underpin a first-class and effective regulatory framework, but also on how the UK’s approach may differ somewhat from that adopted by the EU and the need for flexibility.

While this top-down approach seems appropriate from a strategic perspective, there will inevitably be issues that need to be addressed immediately. For instance, the UK has already stated that it won’t be implementing the EU’s Central Securities Depositories Regulation, and that Securities Financing Transactions Regulation will diverge from the EU regulation in that it won’t be a requirement for non-financial counterparties.

It’s now clear that the UK will – not may – diverge from EU financial regulation, especially in prudential regulation (Basel III). The UK Treasury’s consultation on the future financial framework should provide some important clues about what to expect.

It’s also going to be important to keep an eye on venues and equivalence. In a best-case scenario, there will be full equivalence between EU and UK trading venues by the end of the transition period, but this is by no means certain. In the meantime, trading venues and most market participants have already taken actions to minimise the impact on cross-border activities.

- For a high-level snapshot of life after Brexit click here

- For insights on Brexit resiliency click here